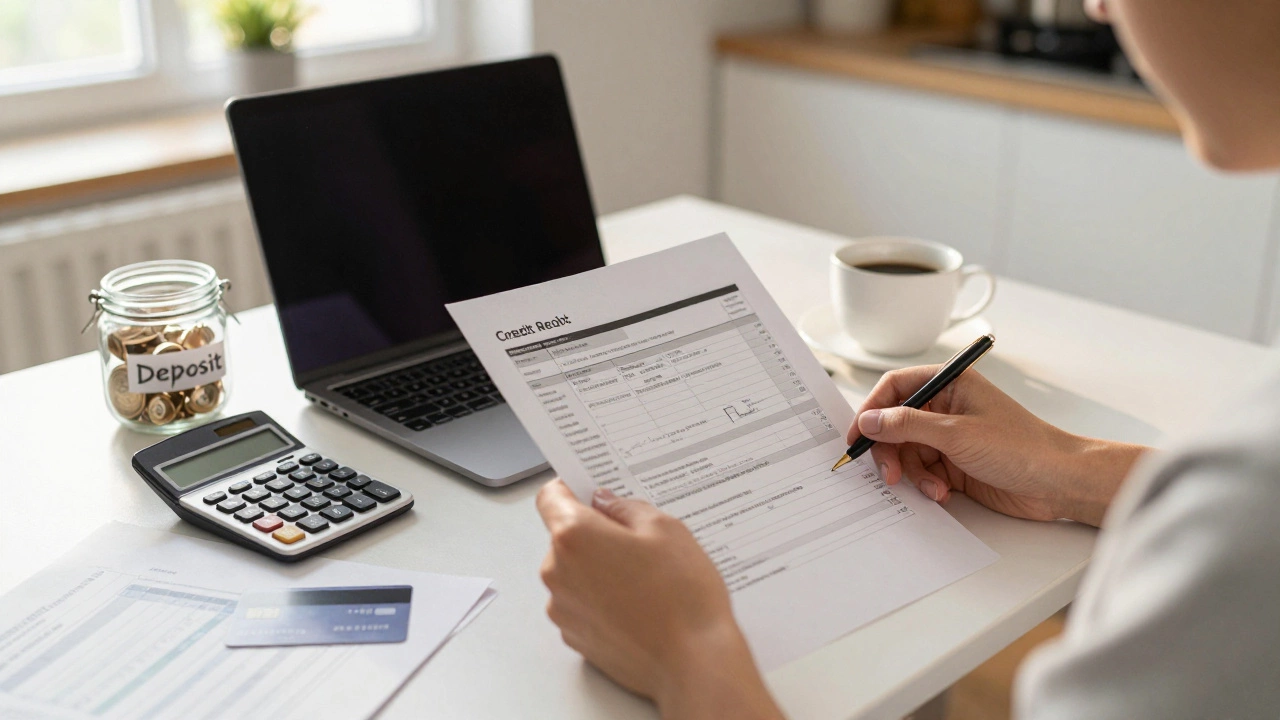

Debt Consolidation: Simple Steps to Combine and Cut Your Debt

Got a bunch of credit‑card bills, a student loan, and maybe a personal loan? It can feel like you’re juggling too many due dates. Debt consolidation is a way to roll those balances into one payment, often at a lower interest rate. The idea is simple: fewer bills, lower cost, and a clearer path to being debt‑free.

How Debt Consolidation Works

First, you check how much you owe in total. Add up the balances, interest rates, and monthly payments. Next, you look for a single loan or a balance‑transfer credit card that can cover most or all of that amount. If the new loan’s interest rate is lower than the average of your current rates, you’ll save money every month.

There are three common ways to consolidate:

- Personal loan: A fixed‑rate loan from a bank or online lender. You get a lump sum, pay it back over a set term, and the interest stays the same.

- Balance‑transfer credit card: You move high‑interest card balances onto a card that offers 0 % intro APR for a set period. You need good credit to qualify.

- Home equity loan or line of credit: If you own a home, you can borrow against its value. The rates are usually low, but you risk losing the house if you miss payments.

Whichever route you pick, the goal is to end up with one payment that’s easier to manage and cheaper overall.

Choosing the Right Consolidation Option

Start by checking your credit score. A higher score opens more low‑rate offers. If your score is low, a personal loan might be tougher to get, but a balance‑transfer card could still work if you have a decent score.

Next, compare fees. Some loans charge an origination fee, and balance‑transfer cards often have a 3‑5 % fee on the amount you move. Add those costs to the interest you’ll pay to see which option truly saves you money.

Also think about the repayment timeline. A longer loan means lower monthly payments but more interest over time. A shorter term saves interest but requires higher payments. Pick a term that fits your budget without stretching you thin.

If you have student loans, look at federal repayment plans first. Income‑Driven Repayment (IDR) can lower monthly payments without a new loan. Some people combine a personal loan with their student debt to get a single payment, but they lose federal protections like deferment and forbearance.

Finally, create a budget that shows where every pound goes. Cut any non‑essential spend, and direct the savings toward your new single payment. Seeing the total amount you owe shrink each month can be a big motivation boost.

Debt consolidation isn’t a magic fix; it works best when you pair it with disciplined spending. Keep tracking your expenses, avoid taking on new high‑interest debt, and stick to the repayment schedule. In a few years, you’ll have one cleared account and a lot more peace of mind.

Will Debt Consolidation Hurt Your Credit Score? The Real Impact Explained

Discover how debt consolidation impacts your credit score. Learn about the temporary dip from hard inquiries, the long-term benefits of lower utilization, and strategies to rebuild your credit effectively.

Debt Consolidation vs. Debt Settlement: Which One Actually Works?

Confused between debt consolidation and debt settlement? Learn the key differences, impact on credit scores, and how to choose the right path for your financial situation.

Can I Release Equity to Pay Off Debt? Here’s What You Need to Know

Releasing equity to pay off debt can lower monthly payments but risks losing your home’s value over time. Learn when it helps, when it hurts, and what alternatives exist in Australia.

Will a Debt Consolidation Ruin My Credit? The Real Impact Explained

Debt consolidation won't ruin your credit if you use it wisely. It can actually boost your score by lowering credit utilization and simplifying payments. Learn how it works, when it helps, and the mistakes that make things worse.

What Credit Score Do You Need for a Consolidation Loan in Australia?

Find out what credit score you need for a consolidation loan in Australia, how lenders judge your application, and how to improve your chances - even with bad credit.

What Happens After 7 Years of Not Paying Debt in Australia

After seven years of not paying debt in Australia, legal action becomes impossible and credit listings disappear. But the debt still exists-here’s what really happens, what collectors can still do, and how to rebuild your finances.

Can I Buy a House After Debt Consolidation? Here's What Actually Happens

Buying a house after debt consolidation is possible-but only if you've rebuilt your finances over 6-12 months. Learn what lenders look for, how your credit score recovers, and how to get approved.

How to Put All Your Debt Into One Payment: A Simple Guide to Debt Consolidation

Learn how to combine all your debts into one simple payment using debt consolidation. Discover the best methods, avoid common traps, and find out if it’s right for your situation in 2025.

How Much Debt Is Too Much to Consolidate? A Realistic Guide for Australians

Learn when debt consolidation helps or hurts. Find out your debt-to-income ratio, avoid common traps, and discover if you're ready to truly get out of debt - not just rearrange it.

How to Pay Off $30,000 Debt in One Year

Learn how to pay off $30,000 in debt in one year using proven strategies like debt consolidation, the avalanche method, side income, and strict budgeting - without needing a windfall.

Should You Take Equity Out of Your House? Pros, Cons & Smart Tips

Learn when taking equity out of your home is smart, compare loan options, weigh pros and cons, and get a clear checklist to decide if equity release fits your financial plan.

Does Debt Consolidation Hurt Your Credit? What Happens To Your Score

Worried if debt consolidation hurts your credit? This guide breaks down how it affects your score—both the good and the bad—so you know what to expect.