Credit Impact Calculator

How Debt Consolidation Affects Your Credit

Based on your current debt situation, this tool estimates the potential impact on your credit score. Remember: your actions after consolidation matter most.

Estimated Credit Score Impact

Key factors in your calculation:

- Credit utilization reduction: +35 points

- Hard inquiries: -25 points

- New account age impact: -10 points

Your Credit Score Path

Based on the article, here's what you can do to maximize benefits:

Pay on time

Your on-time payments will rebuild trust and boost your score over time.

Keep credit utilization below 30%

Maintain low utilization to prevent score drops.

Avoid new credit applications

Don't apply for new credit during consolidation.

People often hear that debt consolidation is a quick fix for juggling too many bills. But the big question hanging over it is: will a debt consolidation ruin my credit? The short answer? Not if you do it right. But it can hurt - and that’s where most people get tripped up.

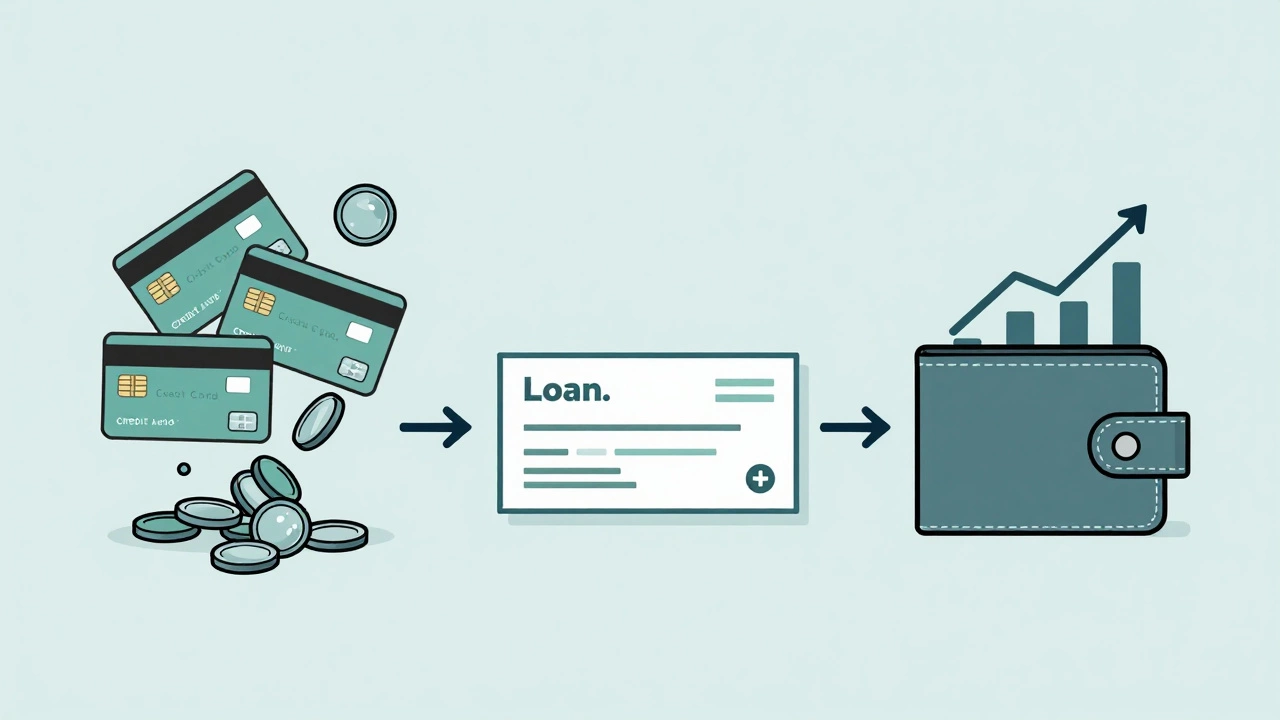

How Debt Consolidation Actually Works

Debt consolidation isn’t magic. It’s a simple idea: you take out one new loan - usually with a lower interest rate - and use it to pay off several smaller debts. Now instead of juggling three credit cards, a medical bill, and a personal loan, you’ve got one monthly payment. Sounds easy, right? But the process has hidden steps that affect your credit in ways most people don’t expect.

There are two main ways people consolidate debt: a debt consolidation loan or a balance transfer credit card. Some also use a nonprofit credit counseling program that negotiates lower payments with creditors. Each path has different effects on your credit report.

When Debt Consolidation Helps Your Credit

Here’s the truth most lenders won’t tell you: if you’re behind on payments or maxed out on cards, your credit score is already taking a beating. Consolidating can actually start to fix that.

Let’s say you have three credit cards, all at 95% of their limit. That’s a credit utilization rate of 95%. Credit scoring models like FICO and VantageScore treat high utilization like a red flag - even if you pay on time. Paying those off with a consolidation loan drops your utilization to near zero. That one change alone can boost your score by 40 to 80 points.

Also, having one payment instead of five makes it way easier to stay on time. Missed payments drag your score down faster than anything else. One late payment can cost you 100+ points. Consolidation reduces that risk.

And here’s something surprising: closing old credit card accounts after paying them off doesn’t hurt as much as people think. Yes, it shortens your credit history a bit. But if your overall credit usage drops dramatically, the gain outweighs the loss.

When Debt Consolidation Hurts Your Credit

Now, the flip side. Debt consolidation can ding your score - but only if you make mistakes.

Hard inquiries - when a lender checks your credit to approve your loan - each knock your score by 5 to 10 points. If you apply for three different loans in a month, that’s 30 points gone. And those inquiries stay on your report for two years, even if you don’t get approved.

Another problem: opening a new loan. A brand-new account lowers your average account age. Credit scoring models like long-standing accounts. If you’ve had a credit card for 12 years and open a new consolidation loan, your average account age drops. That can cost you 10 to 20 points.

Worst case? You consolidate, pay off your cards, then start charging again. That’s called debt cycling. You end up with the same debt plus a new loan. Your credit utilization spikes again, and now you’ve got two sets of debt. That’s a recipe for disaster.

What Happens to Your Credit Report?

Your credit report doesn’t just show your score. It shows the history of every account. Here’s how consolidation shows up:

- Debt consolidation loan: Appears as a new installment loan. Your old accounts show as "paid in full" - which looks good.

- Balance transfer card: Your old cards show zero balances. The new card shows the transferred amount. High utilization on the new card can hurt if you don’t pay it down fast.

- Credit counseling program: Some reports note you’re enrolled in a debt management plan. This doesn’t directly lower your score, but some lenders see it as a red flag.

None of these are permanent. The new loan stays on your report for up to 10 years after it’s closed. But if you pay it on time, it becomes a positive factor. Timely payments over time rebuild trust with lenders.

Real-World Example: Sarah’s Story

Sarah, 38, from Brisbane, had $22,000 in credit card debt across four cards. Her credit score was 592. She was paying $1,100 a month just to keep up. Her interest rates ranged from 19% to 24%.

She got a debt consolidation loan for $22,000 at 9.5% over five years. Her new payment? $460. She closed all four cards.

Her credit score dropped 38 points the first month - thanks to the hard inquiry and new account. But within four months, her utilization dropped from 94% to 3%. Her score jumped to 681. By year two, she’d paid off half the loan and her score hit 745. She’s now applying for a car loan.

She didn’t ruin her credit. She fixed it.

What to Avoid at All Costs

Here are the three biggest mistakes people make:

- Applying for multiple loans - shop around, but do it in a 30-day window. Credit scoring models treat multiple inquiries for the same type of loan as one.

- Using old credit cards again - freeze them, cut them up, or set up alerts so you can’t spend over $50.

- Choosing a loan with a longer term just to lower the payment - yes, your monthly bill goes down, but you pay thousands more in interest. Always compare total cost, not just monthly payment.

Who Shouldn’t Consolidate Debt?

Debt consolidation isn’t for everyone. If you’re:

- Still spending more than you earn

- Not ready to change your spending habits

- Unable to qualify for a better interest rate than what you’re already paying

…then consolidation won’t help. It might even make things worse by giving you more credit to mess up.

In those cases, a budgeting plan with a nonprofit credit counselor (like National Foundation for Credit Counseling) might be better. They don’t touch your credit score, and they help you build real habits.

The Bottom Line

Will a debt consolidation ruin your credit? No - unless you treat it like a free pass to keep spending. Done right, it’s one of the most effective tools to rebuild credit. The score dip is temporary. The payoff - lower interest, one payment, and a path to being debt-free - lasts years.

Track your progress. Use free tools like Credit Karma or your bank’s credit score dashboard. Watch your utilization drop. Watch your payment history improve. That’s how credit gets fixed - not by magic, but by consistency.

Does debt consolidation show up on my credit report?

Yes. A debt consolidation loan appears as a new installment loan. Your old accounts will show as "paid in full" or "closed with zero balance." If you use a balance transfer card, the new card will show the transferred balance, and your old cards will show $0. Credit counseling programs may note your enrollment in a debt management plan. None of these are hidden - lenders see them all.

How long does debt consolidation hurt my credit score?

The dip usually lasts 3 to 6 months. The hard inquiry from applying for the loan drops your score slightly and stays for two years. The new account lowers your average credit age, which can affect you for up to a year. But once you start making on-time payments and reduce your credit utilization, your score begins climbing. Most people see improvement within four months if they don’t take on new debt.

Can I consolidate debt with bad credit?

It’s harder, but not impossible. If your credit score is under 600, you may still qualify for a secured loan, a loan with a co-signer, or a debt management plan through a nonprofit agency. Avoid payday lenders or "no credit check" consolidation offers - they charge crazy fees and trap you in deeper debt. Focus on improving your score first: pay down balances, dispute errors, and avoid new credit applications for 3 to 6 months.

Is a balance transfer card better than a loan for consolidation?

It depends. A balance transfer card is great if you can pay off the full balance before the 0% intro rate ends - usually 12 to 21 months. But if you can’t, you’ll get hit with high interest. A personal loan gives you a fixed rate and fixed term. If you need 3+ years to pay off debt, a loan is usually cheaper. Watch out for transfer fees - they’re typically 3% to 5% of the amount transferred.

Will closing credit cards after consolidation hurt my score?

It can, but not as much as you think. Closing cards reduces your total available credit, which can raise your utilization rate. But if you’re paying off high-balance cards first, the drop in utilization usually outweighs the loss of available credit. The bigger issue is losing older accounts - they help your credit history length. If possible, keep one or two old cards open with tiny balances and set up autopay for $5 a month to keep them active.