Personal Loan Monthly Payment Calculator

Let’s cut through the noise: if you’re asking how much you’d pay each month on a $5000 personal loan, you’re not just looking for a number-you’re trying to figure out if you can actually afford it. And that’s smart. Too many people grab a loan without knowing what’s coming, then get stuck in a cycle of missed payments and fees. So let’s get real about what that $5000 loan really costs each month.

It’s not just the $5000

You’re not just paying back $5000. You’re paying back $5000 plus interest. And interest? It changes everything. The difference between a 9% rate and a 17% rate on a $5000 loan can mean hundreds of dollars extra over the life of the loan-and that adds up fast in your monthly budget.

In Australia, personal loan rates vary widely. As of early 2026, the average rate for a secured personal loan is around 9.5%, while unsecured loans (which don’t need collateral) sit between 12% and 18%. If you’ve got decent credit, you might land closer to 9%. If your score is shaky? You could be looking at 17% or higher. That’s why shopping around isn’t optional-it’s essential.

Term length makes or breaks your budget

The length of your loan-called the term-has a huge impact on your monthly payment. Most personal loans in Australia run from 1 to 7 years. Shorter terms mean higher payments but less interest. Longer terms mean lower payments but more total cost.

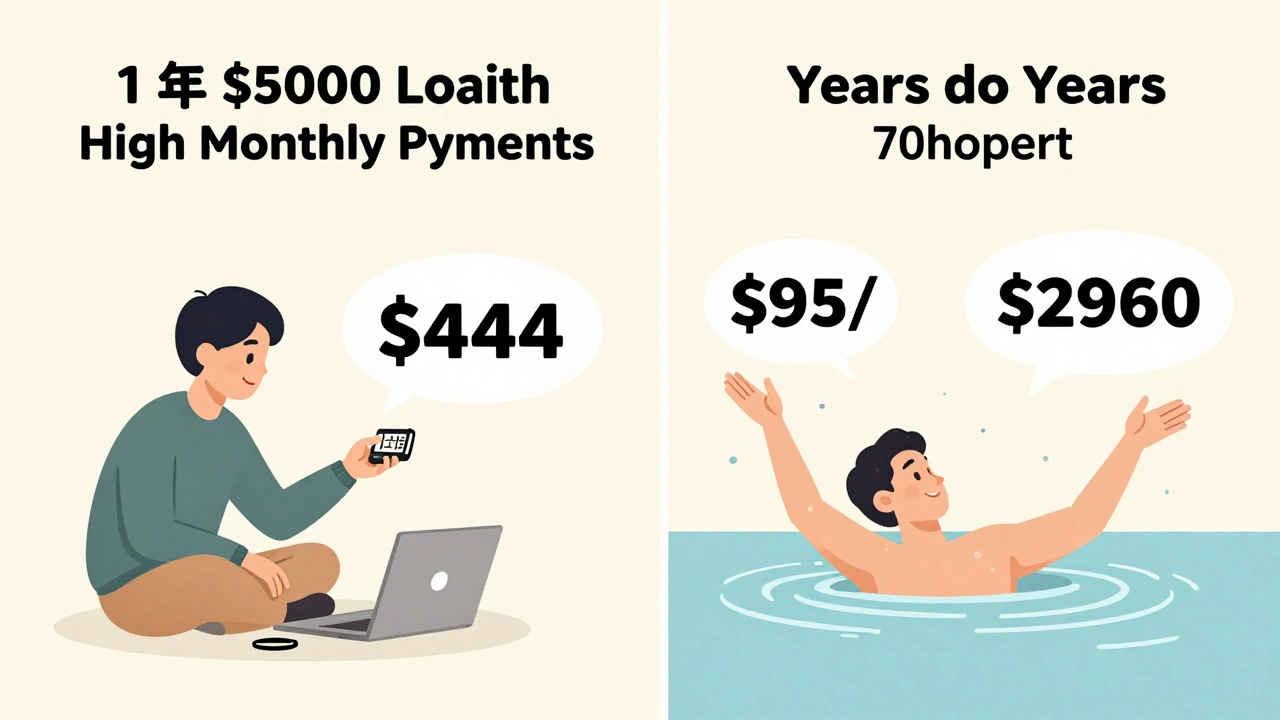

Here’s what that looks like for a $5000 loan at 12% interest:

| Loan Term | Monthly Payment | Total Interest Paid | Total Repaid |

|---|---|---|---|

| 1 year (12 months) | $444 | $328 | $5,328 |

| 2 years (24 months) | $235 | $640 | $5,640 |

| 3 years (36 months) | $168 | $1,048 | $6,048 |

| 5 years (60 months) | $116 | $1,960 | $6,960 |

| 7 years (84 months) | $95 | $2,960 | $7,960 |

See how the 7-year option cuts your payment nearly in half compared to the 1-year option? But look at the total you end up paying: nearly $3,000 in interest. That’s more than half the original loan amount. That’s not a bargain-it’s a trap if you’re not careful.

What’s realistic for most Australians?

In Brisbane, where I live, most people who take out a $5000 personal loan go with a 3-year term. Why? It balances affordability with cost. The $168 monthly payment is manageable for a lot of households, and the total interest ($1,048) is still under 25% of the loan amount.

But here’s the thing: $168 a month sounds fine until you realize it’s not just one payment. You’ve got rent, electricity, groceries, phone bills, maybe a car payment. Add in unexpected costs-a broken fridge, a medical co-pay, a flat tire-and that $168 becomes a pressure point. That’s why I always tell people: don’t just check if you can afford the payment. Ask yourself: can you afford it if something goes wrong?

Hidden costs you can’t ignore

Some lenders advertise "low rates" but sneak in fees that blow out your total cost. Watch out for:

- Application fees-some charge $150-$300 just to process your loan.

- Monthly service fees-even if your rate is low, a $5/month fee adds $360 over 6 years.

- Early repayment penalties-some lenders charge you if you pay off early to avoid losing interest. That’s a trap.

- Default fees-miss a payment? You could pay $35-$75 extra.

Always ask: "What are all the fees I’ll pay over the life of this loan?" If they hesitate or say "it’s in the fine print," walk away. A good lender won’t hide costs.

What if you can’t get approved?

If your credit score is below 600, you might get turned down-or offered a loan with a rate over 20%. That’s not a loan. That’s a debt spiral.

Don’t panic. Instead:

- Check your credit report for errors. Many Australians have mistakes on their reports that drag their score down.

- Apply for a secured loan. Put up something valuable-like a car or savings account-as collateral. That can slash your rate.

- Ask a family member to co-sign. It’s not ideal, but it can open doors.

- Try a credit union. They often have better rates than big banks for people with average credit.

Is a 00 loan even the right move?

Before you sign anything, ask: why do I need this loan? If it’s for a car, a medical bill, or urgent home repairs-then yes, it makes sense. But if it’s for a holiday, new clothes, or to cover overspending? That’s not a loan. That’s a financial mistake.

There’s a reason personal loans have a bad reputation. Too many people use them like credit cards. But unlike credit cards, personal loans have fixed payments and fixed terms. That’s good-if you’re disciplined. It’s deadly if you’re not.

If you’re unsure, try this: take the monthly payment amount and put it into a savings account for 30 days. If you can live without it, maybe you don’t need the loan. If you can’t, then you’ve got bigger budget issues to fix first.

Bottom line: Know your numbers

There’s no single answer to "how much would a monthly payment be on a $5000 personal loan?" It depends on your interest rate, your term, and your fees. But here’s the rule of thumb most Australians use:

- For a 3-year term at 12%, expect $168 per month.

- For a 5-year term at 15%, expect $120 per month.

- For a 1-year term at 9%, expect $435 per month.

Use a free personal loan calculator from ASIC’s Moneysmart website to plug in your exact numbers. Don’t guess. Don’t trust a lender’s verbal estimate. Do the math yourself.

And remember: the lowest monthly payment isn’t always the best deal. The goal isn’t to make the payment fit your budget-it’s to make sure you’re not paying twice as much as you need to.