Term vs Whole Life Insurance Calculator

Your Insurance Details

Your Results

Invest the Difference

If you invest the $265.00 monthly difference at 7% annual return:

Total Investment Value After 30 Years: $351,860.00

*(Assumes 7% annual return with monthly compounding)

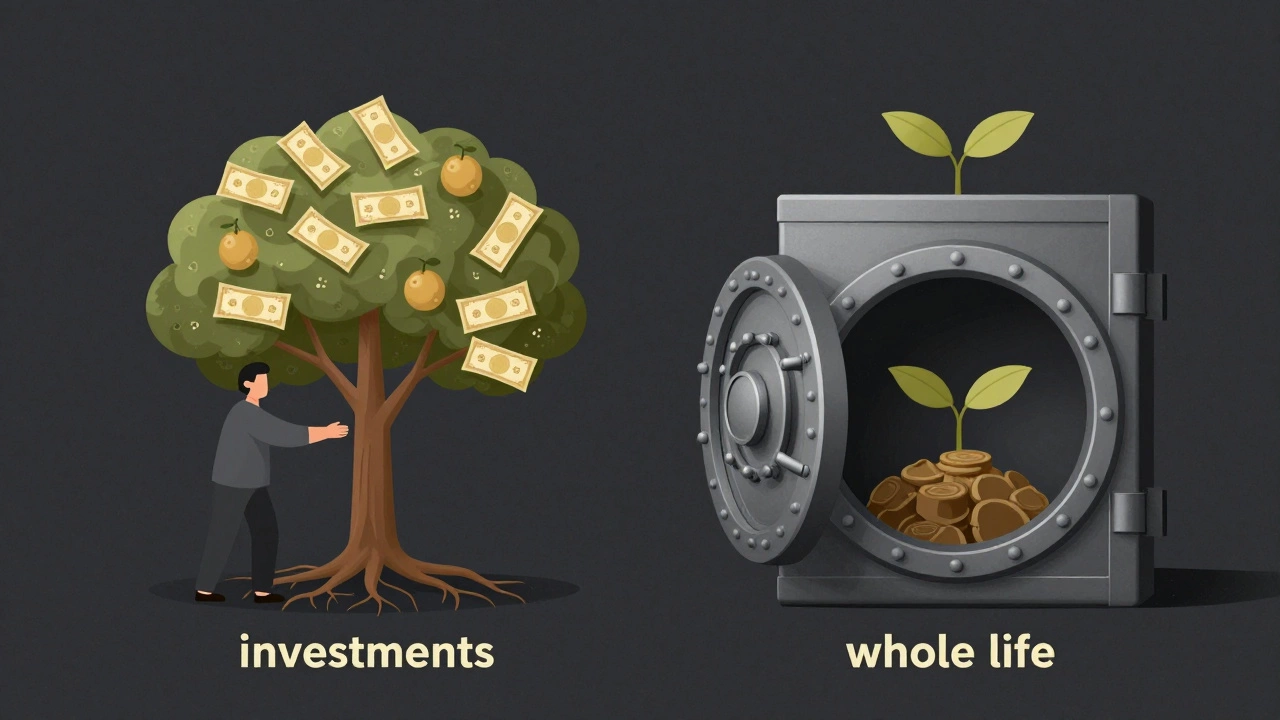

When you’re buying life insurance, the biggest decision isn’t about coverage amount or payment frequency-it’s choosing between term life insurance and whole life insurance. Most people don’t realize these aren’t just different products-they’re designed for completely different goals. One is a financial tool. The other is a savings plan dressed up as protection.

Term Life Insurance: Pure Protection, No Frills

Term life insurance gives you coverage for a set number of years-usually 10, 20, or 30. If you die during that time, your beneficiaries get the death benefit. If you outlive the term? The policy ends. No payout. No cash value. Just like car insurance-you pay for protection while you need it.

Here’s what you actually get with term life:

- Low monthly premiums-often under $30 a month for a healthy 35-year-old buying a $500,000 policy

- Simple, no-nonsense coverage

- Fixed premiums for the term length

- No investment component

People who choose term life are usually focused on one thing: protecting their family if something happens before the kids are grown or the mortgage is paid off. If you’re 32, have two young children, and a $400,000 home loan, term life makes sense. You’re not trying to build wealth-you’re trying to make sure your family doesn’t lose their home.

Term policies can be renewed after the term ends, but the premiums jump-sometimes by 300% or more. That’s why most people plan to outgrow the need for coverage by the time the term ends.

Whole Life Insurance: Insurance Plus Savings (But at a Cost)

Whole life insurance lasts your entire life-no expiration date. It also builds cash value over time. That cash value grows slowly, tax-deferred, and you can borrow against it or withdraw it. But here’s the catch: it’s expensive.

For the same $500,000 death benefit, a healthy 35-year-old might pay $250-$400 a month for whole life. That’s eight to ten times more than term life.

What are you paying for? Part of that premium goes to the death benefit. The rest goes into a savings account the insurance company controls. The growth is guaranteed, but it’s typically around 2% to 4% per year-far below what you could earn in a low-cost index fund.

Some agents sell whole life as an “investment.” But it’s not. It’s a slow, expensive way to save. If you want to invest, open a brokerage account. If you want insurance, buy term.

When Whole Life Might Make Sense

There are a few cases where whole life isn’t just a bad idea-it’s the only idea.

- You have a permanent need for coverage-like a business partnership where your death triggers a buyout agreement

- You’re in a high-income bracket and have maxed out all other tax-advantaged accounts (super, investment bonds, etc.)

- You need to leave a tax-free inheritance to heirs who won’t be able to manage large sums of money

- You have a disabled dependent who’ll need lifelong financial support

In those cases, the cash value feature and guaranteed death benefit can be useful. But even then, most financial advisors recommend using other tools first-like trusts or specialized insurance products designed for estate planning.

Term Life Wins 95% of the Time

Let’s say you buy a 30-year term policy for $35 a month. That’s $420 a year. Over 30 years, you’ll pay $12,600 total.

Now, if you bought whole life for the same death benefit? You’ll pay about $300 a month-that’s $3,600 a year. Over 30 years, that’s $108,000.

Now imagine you take the $3,200 difference each year (the gap between whole life and term) and invest it in a low-cost index fund earning 7% annually. After 30 years? You’d have over $350,000-more than enough to replace the death benefit and then some.

This is called the “buy term and invest the difference” strategy. It’s not a theory. It’s been proven by actuaries, financial planners, and decades of real-world data. The people who win at life insurance aren’t the ones who pay the most-they’re the ones who pay the least and invest the rest.

What Happens If You Outlive Your Term Policy?

Many people worry: “What if I still need coverage after 20 years?” That’s a good question.

By age 55, most people have paid off their mortgage, their kids are independent, and their income is stable. They don’t need $500,000 in life insurance anymore. They need retirement savings.

But if you still have debts, dependents, or a business to protect, you can renew your term policy. Or better yet-you can buy a new one. Premiums will be higher because you’re older, but they’ll still be far lower than whole life.

There’s also a product called “convertible term life.” It lets you switch your term policy to permanent coverage without a medical exam. That’s useful if your health declines later in life. But most people don’t need it. Only 10-15% of term policies are ever converted.

Red Flags: What Agents Won’t Tell You

Whole life insurance salespeople often use emotional language: “You’re leaving your family behind,” or “This is the only way to guarantee your legacy.”

Here’s what they don’t say:

- The cash value is locked in-you can’t access it without paying interest or reducing your death benefit

- Early withdrawals can trigger taxes and penalties

- The policy’s “dividends” aren’t guaranteed-they’re projections based on the company’s performance

- Commission payouts for whole life are 5-10 times higher than for term life

That’s why you’ll hear more about whole life from agents than from financial planners. It’s not because it’s better-it’s because it pays better.

What Should You Do?

Ask yourself these three questions:

- Do I need coverage for a limited time-like until my kids are grown or my mortgage is paid off? If yes, get term.

- Do I have a permanent need for insurance and have already maxed out all other savings and investment options? If yes, talk to a fee-only advisor before buying whole life.

- Am I being told this is an “investment”? If yes, walk away.

Term life insurance is the smart choice for 95% of people. It’s affordable, transparent, and does exactly what it says: protects your loved ones if you die too soon.

Whole life insurance isn’t evil. But it’s not the solution most people think it is. It’s a complex product sold with emotional appeals. And in most cases, it’s a waste of money.

If you’re buying life insurance to protect your family-don’t overpay. Get term. Invest the rest. Build real wealth. That’s how you win.

Is term life insurance enough for most people?

Yes. Term life insurance covers the most common reasons people need life insurance: replacing lost income, paying off a mortgage, or funding a child’s education. For 90% of families, term coverage lasting until age 65 or 70 is more than enough. The key is matching the term length to your financial responsibilities-not your fears.

Can I switch from whole life to term life later?

You can cancel a whole life policy at any time, but you’ll likely lose most of the cash value-especially if you’ve held it less than 10 years. Surrender charges can eat up 30-50% of your savings. If you’re stuck with whole life, consider keeping it for a few more years to recover some value, then replace it with term. But don’t cancel abruptly.

Why do financial advisors rarely recommend whole life?

Because it’s inefficient. A fee-only advisor earns based on your results, not commissions. They’ll see that whole life ties up thousands in low-return cash value while charging high fees. They’ll recommend investing that money elsewhere-like in low-cost ETFs, super contributions, or property-where returns are higher and control is yours.

Does whole life insurance help with estate planning?

It can, but only in specific situations. If your estate is worth more than $1 million (in Australia, the threshold is much higher for tax purposes), and you want to leave a tax-free payout to heirs, whole life can help. But trusts, life insurance trusts, and super death benefit nominations are usually better tools. Whole life is rarely the first choice.

Are there any Australian-specific rules for term vs whole life?

In Australia, life insurance is often held inside superannuation. Term life through super is usually cheaper and tax-effective. Whole life policies outside super are rare here-most are imported from the U.S. and come with high fees. Australians are better off using term insurance inside super for income replacement and standalone policies for larger needs like business protection.