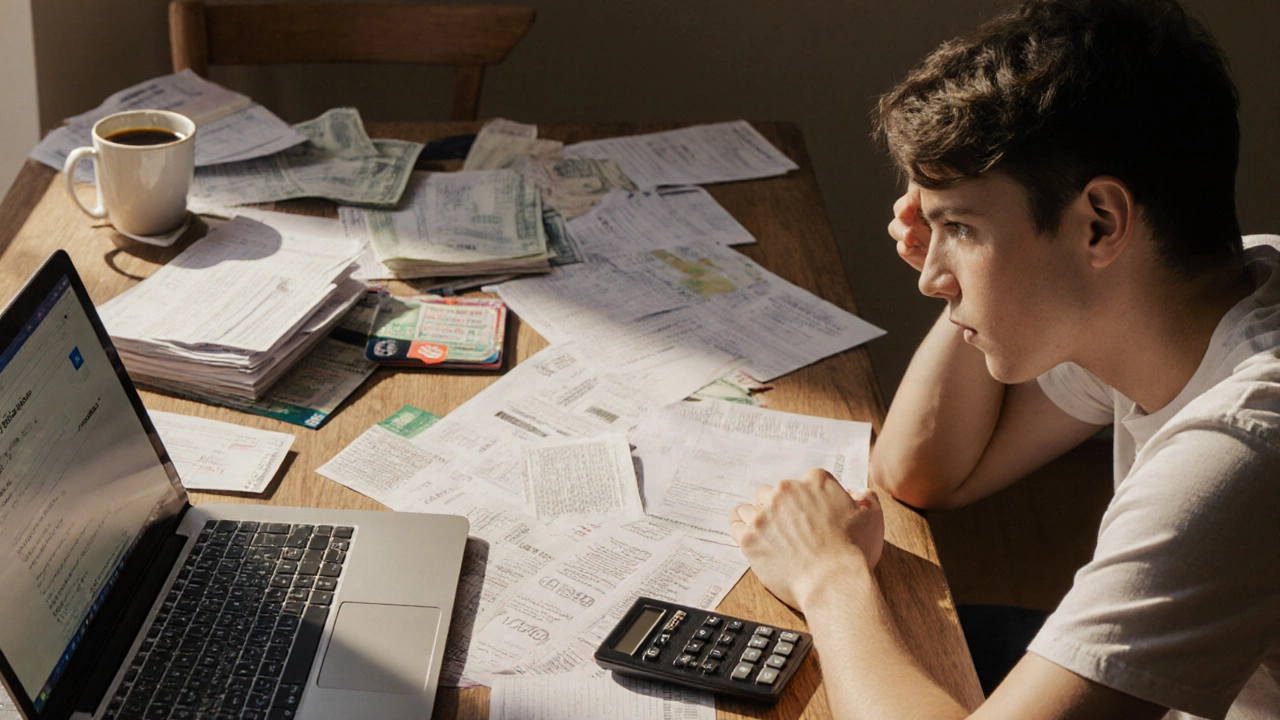

Debt Consolidation Impact: What It Means for Your Credit and Finances

When dealing with debt consolidation impact, the way combining multiple debts into a single loan changes your credit profile, payment schedule, and overall financial health. Also known as debt consolidation effect, it can influence both short‑term cash flow and long‑term credit standing. Debt consolidation impact isn’t a vague buzzword; it’s a measurable shift in how lenders see you, how much you pay each month, and how quickly you can erase debt.

Key Factors That Shape the Impact

Your credit score, a three‑digit number that predicts loan risk is usually the first metric that moves. A fresh personal loan can cause a short‑term dip because of a hard inquiry and the new account’s age, but it also offers a chance to lower your utilization ratio, which may boost the score over time. Choosing the right personal loan, the single product that replaces several credit cards or smaller loans matters – lower interest, fixed repayment terms, and transparent fees keep the balance between cost and credit benefit. Meanwhile, working with a reputable debt relief, service that negotiates with creditors or consolidates debt for you can smooth the process, but it adds another layer of reporting that lenders watch. In short, the debt consolidation impact encompasses credit‑score changes, requires careful loan selection, and is influenced by the quality of any debt‑relief partner you pick.

Practically, start by pulling your credit report and noting the current score, total balances, and interest rates. Compare at least three loan offers – look beyond the headline rate and check fees, repayment length, and whether the lender reports to major bureaus. If you have high‑interest credit‑card debt, a lower‑rate loan can shave off months of interest and improve utilization, which nudges the score upward. If you’re unsure about managing a single payment, consider a debt‑relief company that offers a structured payment plan; just verify their accreditation and read reviews before signing. Keep an eye on the post‑consolidation period: make payments on time, avoid opening new credit lines, and monitor your score monthly. These steps turn the debt consolidation impact from a potential risk into a strategic advantage.

Below you’ll find curated articles that dig deeper into each of these angles – from how consolidation affects credit, to tips on picking the right loan, to evaluating debt‑relief firms. Use them as a roadmap to decide whether consolidating your debt will boost your financial picture or create new challenges.

Negative Effects of Debt Consolidation Explained

Explore the hidden costs, credit‑score impact, longer terms, and stress that debt consolidation can bring, plus tips to avoid the pitfalls.