Pay Off Debt Fast: Proven Ways to Get Out of Debt Without Breaking Your Budget

When you’re trying to pay off debt fast, a financial strategy focused on reducing high-interest obligations quickly to regain control of your money. Also known as debt elimination, it’s not about cutting corners—it’s about working smarter with what you already have. Most people think they need a big raise or a windfall to get out of debt, but that’s not true. The real game-changer is knowing which debts to attack first, how to stop new ones from piling up, and what tools actually move the needle.

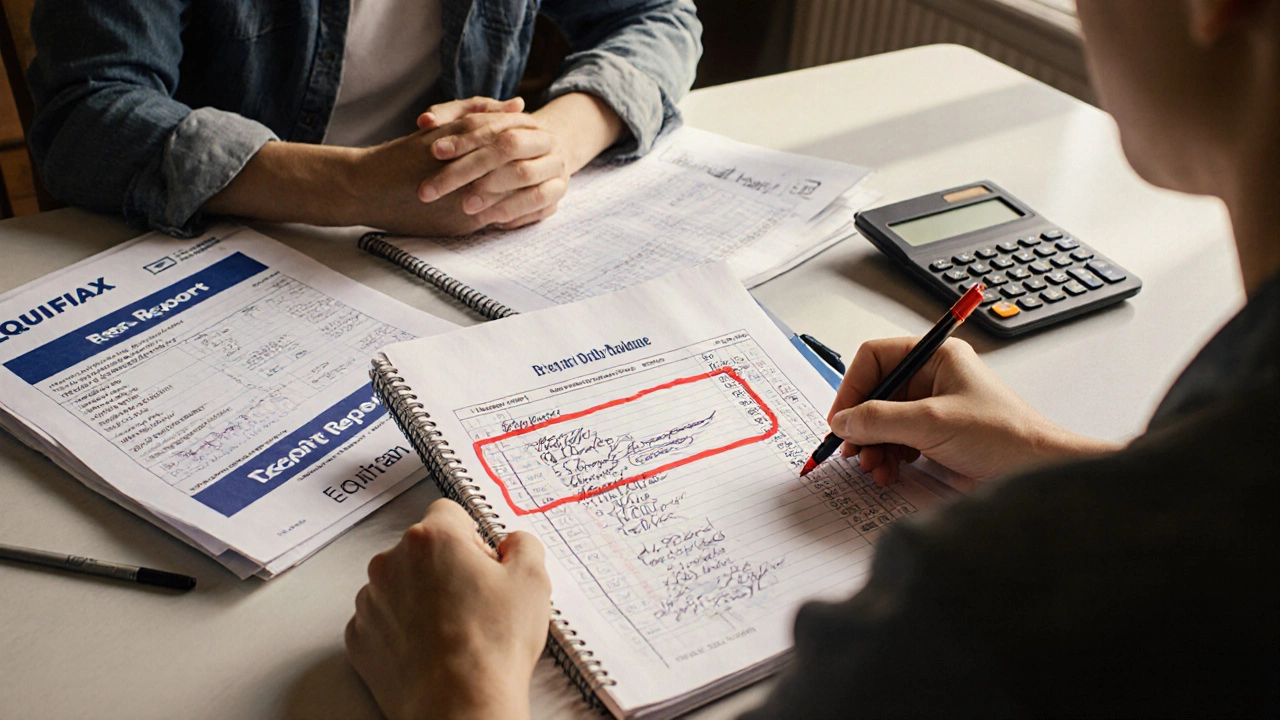

One of the biggest mistakes people make is mixing up debt consolidation, a method of combining multiple debts into a single loan with lower interest or better terms. Also known as debt refinancing, it can help—but only if you don’t keep spending the same way afterward. A lot of folks use a home equity loan or a balance transfer card to roll their credit cards into one payment, then turn around and charge up the cards again. That doesn’t pay off debt—it just moves it around. What works is pairing consolidation with a solid budgeting, a system for tracking income and expenses to ensure you’re spending less than you earn. Also known as money management, it’s the foundation of every successful debt plan. You don’t need a fancy app. Start with pen and paper. Write down every dollar you make and every dollar you spend for 30 days. You’ll be shocked where the money goes. That’s where you find the room to pay more than the minimum.

Your credit score, a three-digit number lenders use to judge how risky you are to lend money to. Also known as FICO score, it’s not just a number—it’s your financial reputation. Paying off debt fast doesn’t just save you interest; it lifts your score. And a higher score means better rates on future loans, lower insurance premiums, even better cell phone deals. But here’s the catch: your score doesn’t jump just because you pay your bills. It rises when you lower your credit utilization—meaning you owe less compared to what you’re allowed to borrow. If you’ve got $5,000 in credit limits and you owe $4,500, you’re in danger zone. Pay it down to $1,500, and your score will start climbing. That’s not magic. That’s math.

You’ll find posts here that show you how to use home equity without refinancing, why debt consolidation can backfire, and how to build a budget that actually sticks. No fluff. No get-rich-quick schemes. Just real steps people in the UK have used to ditch debt—some in under two years. Whether you’re juggling credit cards, medical bills, or payday loans, the path out is the same: know your numbers, attack the right debt first, and never stop tracking your progress. What you’re about to read isn’t theory. It’s what works when you’re tired of feeling stuck.

How to Pay Off $30,000 Debt in One Year

Learn how to pay off $30,000 in debt in one year using proven strategies like debt consolidation, the avalanche method, side income, and strict budgeting - without needing a windfall.