Car Loan APR & Total Cost Calculator

Loan Details

Your Results

Impact of Dealer Markup

By adding 0% to your rate:

- You pay an extra $0.00 in total interest

- Over 60 months

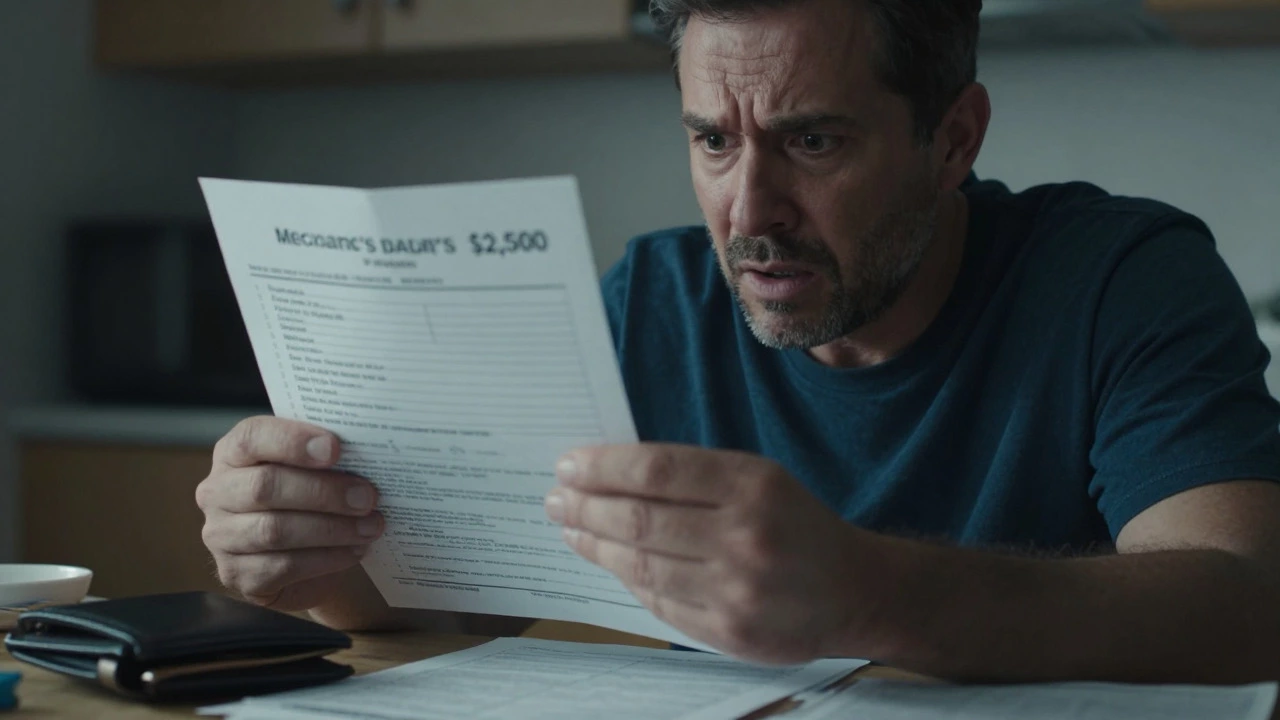

You sit in the dealership office. You’ve done everything right. Your credit score is a numerical expression used to evaluate a consumer's creditworthiness is solid-maybe even excellent. You’re buying a reliable car. Yet, when the finance manager slides that paper across the table, the Annual Percentage Rate (APR) looks like it belongs on a subprime payday loan. It’s confusing, frustrating, and frankly, unfair. If you have good credit, why are you being charged such high interest?

The short answer is that your credit score is just one piece of a much larger puzzle. Lenders don’t look at a single number; they look at risk profiles, market conditions, and their own profit margins. In the current landscape of car finance the process of borrowing money specifically for purchasing a vehicle, several hidden factors can spike your rate even if your credit report looks pristine.

The Hidden Factor: Dealer Markup (The 'Yield Spread')

This is the most common reason you see a higher rate than expected. When you apply for a loan through a dealership, you aren’t necessarily getting the rate directly from the bank. The dealer acts as a broker. They submit your application to multiple lenders. Some lenders offer a base rate, but they also pay the dealer a bonus if they sell you a higher rate. This bonus is called a "yield spread premium" or simply "dealer markup."

Here is how it works in practice. A lender might offer you a base rate of 5%. The dealer adds 2% to that, presenting you with a 7% APR. If you accept without questioning, the dealer pockets that extra 2% as commission. This happens because many buyers focus entirely on the monthly payment amount rather than the total cost of the loan. If you didn’t explicitly ask to buy down the rate or negotiate the interest rate separately from the car price, you likely paid this markup.

Credit Score Nuances: FICO vs. VantageScore

You might check your credit score on a free app and see an 800. That feels great. But here is the catch: that app might be showing you a VantageScore. Most auto lenders use a specific version of the FICO Score, often called FICO Auto Trader Score. These two scoring models weigh data differently.

VantageScore might give you more weight for recent positive behavior, while FICO Auto scores heavily penalize recent hard inquiries or high utilization on revolving accounts. If you applied for a few other loans recently, or if you maxed out a credit card before applying for the car, your FICO Auto score could be significantly lower than your general consumer score. Lenders rely on the FICO Auto model because it has been proven to predict auto loan repayment behavior more accurately. A discrepancy between what you see online and what the lender sees is a frequent source of shock.

| Scoring Model | Primary Use Case | Sensitivity to Recent Activity |

|---|---|---|

| FICO Auto Score | Auto Loan Approval | High (penalizes recent inquiries/utilization) |

| VantageScore 3.0/4.0 | Consumer Apps & General Credit | Medium (focuses on trend analysis) |

| FICO Score 8/9 | Mortgages & Personal Loans | Low to Medium |

Loan Term Length: The Time Trap

Lenders love long terms. You probably do too, because they lower your monthly payment. However, extending your loan term from 60 months to 72, 84, or even 96 months drastically increases your APR. Why? Because risk increases over time. The longer the loan, the higher the chance something goes wrong-mechanical failure, accident, or financial hardship leading to default.

To compensate for this increased risk, lenders charge higher interest rates for longer terms. Additionally, with longer terms, you spend more time underwater (owing more than the car is worth). This negative equity risk makes the loan less attractive to secondary markets if the lender needs to sell the debt. If you opted for a 72-month or 84-month loan to keep payments low, expect your APR to be noticeably higher than the advertised "best rate" which usually applies to 36 or 48-month terms.

The Type of Vehicle Matters More Than You Think

Your credit score isn't the only variable; the collateral is equally important. Lenders view different vehicles as different levels of risk based on depreciation and reliability.

- New Cars: Generally get the lowest rates because they hold value better and have manufacturer warranties.

- Used Cars: Higher rates due to faster depreciation and lack of warranty coverage.

- Leased Vehicles: Often have slightly lower rates than purchased used cars because the lessee must maintain the car in good condition and return it, reducing the lender's risk.

- Exotic or High-Performance Cars: May face higher rates or stricter scrutiny due to niche resale markets and higher insurance costs.

If you are financing a used car that is older than five years, you will rarely qualify for the same promotional rates offered for new vehicles, regardless of your credit score. The asset itself dictates a floor for how low the interest rate can go.

Macroeconomic Factors: The Federal Reserve Influence

In 2026, we are still feeling the aftershocks of the inflation battles fought in the early 2020s. Central banks, including the Federal Reserve in the US and the RBA in Australia, raised benchmark interest rates aggressively to cool down economies. While those rates may have stabilized, they remain higher than the near-zero environment of the previous decade.

Auto loans are tied to these broader economic indicators. When the prime rate rises, the cost of borrowing for banks and credit unions increases. They pass this cost on to you. Even with perfect credit, you cannot escape the baseline cost of money in the economy. If you remember the 3% APR era, that was an anomaly driven by monetary policy, not a reflection of personal creditworthiness alone. Today’s "good" rates are objectively higher than historical averages.

How to Fix It: Negotiating Your Rate Down

If your APR is higher than you want, you have leverage. Here is how to use it.

- Get Pre-Approved Elsewhere: Go to a local credit union or online lender. Get a pre-approved rate. Bring this letter to the dealership. It forces them to compete. If their best offer is worse than yours, ask them to match it.

- Ask for the Base Rate: Explicitly ask the finance manager, "What is the base rate from the lender before any dealer add-ons?" If they hesitate, walk away. You have the right to know the unmarked-up rate.

- Shorten the Term: If possible, choose a shorter loan term. It raises the monthly payment but lowers the APR and total interest paid.

- Check Your Credit Report: Pull your actual FICO Auto score if possible. Ensure there are no errors dragging it down. Dispute any inaccuracies immediately.

- Refinance Later: If you are stuck with a high rate now, drive the car for six months, make all payments on time, and then refinance. Your improved payment history and reduced loan balance can qualify you for a better rate later.

Understanding the Total Cost of Ownership

It is easy to get caught up in the monthly payment. But the APR determines the total amount you pay over the life of the loan. A 1% difference in APR on a $30,000 loan over 60 months can cost you hundreds of dollars. On a longer term, that gap widens significantly.

Always calculate the total interest. If the dealer pushes a higher APR to lower the monthly payment, you are paying for the convenience of a smaller bill with expensive interest. Ask yourself: Is saving $50 a month worth paying $1,000 extra in interest? Usually, the answer is no.

What is considered a good APR for a car loan in 2026?

For borrowers with excellent credit (750+), a good APR for a new car typically ranges between 4% and 6%. For used cars, expect rates between 6% and 8%. Rates above 10% usually indicate either poor credit or significant dealer markup.

Can I negotiate my APR after signing the contract?

Technically, once signed, the contract is binding. However, you can refinance your auto loan with a different lender shortly after purchase. Many lenders allow refinancing after 6-12 months of on-time payments. This effectively replaces your old high-rate loan with a new lower-rate one.

Why do credit unions offer lower rates than dealerships?

Credit unions are non-profit member-owned institutions. They do not have shareholders to pay dividends, so they pass savings back to members in the form of lower interest rates and fees. Dealerships are for-profit entities that earn commissions on loan markups.

Does making a larger down payment lower my APR?

Not directly. The APR is determined by your credit profile and market rates. However, a larger down payment reduces the loan-to-value ratio, which can make you a less risky borrower. Some lenders may offer slightly better terms for loans with lower balances, but the primary benefit is paying less interest overall due to a smaller principal.

Is it better to finance through the dealer or a bank?

It depends on transparency. Financing through a bank or credit union first gives you a benchmark rate. You can then take that offer to the dealer to see if they can beat it. Often, dealers can access exclusive manufacturer incentives, but they may hide these behind high markups. Always compare the final APR and total cost, not just the monthly payment.