Home Equity Calculator

Calculate Your Equity

Enter your home value and current mortgage balance to see your equity and eligibility for a remortgage.

Your Equity Results

Cash-Out Potential: Most lenders allow up to 80% LVR for cash-out remortgages. You may be able to borrow up to $0.

You’ve been paying your mortgage for a few years, and now you’re thinking about remortgaging. Maybe you want a better interest rate, need cash for home repairs, or want to consolidate debt. But here’s the real question: how much equity do you actually need to make it happen?

What Is Equity in Your Home?

Equity is the part of your home you truly own. It’s not what you paid for it. It’s what your house is worth today minus what you still owe on your mortgage.Let’s say you bought a house for $600,000. You put down $120,000 and borrowed $480,000. Now, five years later, your house is worth $750,000. You’ve paid off $80,000 of your loan, so you still owe $400,000. Your equity? $750,000 minus $400,000 = $350,000. That’s your stake in the property.

When you remortgage, lenders don’t care how much you originally borrowed. They care about how much equity you have now. That number tells them how risky you are as a borrower.

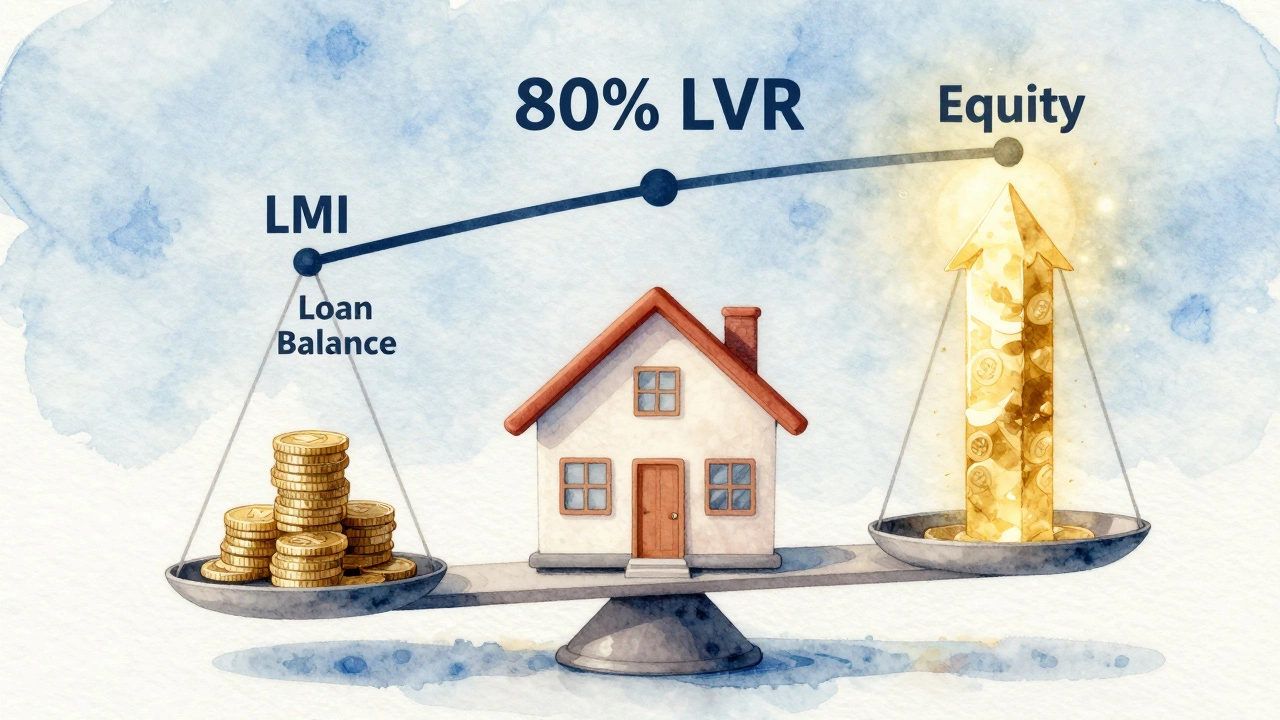

Minimum Equity Requirements in Australia

Most Australian lenders require you to have at least 20% equity in your home to qualify for a standard remortgage. That means your loan-to-value ratio (LVR) can’t be higher than 80%.So if your house is worth $750,000, you need to owe $600,000 or less to hit that 20% equity mark. If you owe $610,000, you’re at 81.3% LVR - and most lenders will say no unless you pay for lenders mortgage insurance (LMI) or meet special criteria.

Some lenders will go as low as 10% equity (90% LVR), but they’re rare. These deals usually come with higher interest rates, extra fees, or stricter income checks. If you’re under 20% equity, you’re not out of the game - but you’ll pay more for the privilege.

Why Does Equity Matter to Lenders?

Banks don’t lend money because they like you. They lend because they need to get it back - plus interest. Equity acts as their safety net.If you default on your loan, the lender can sell your home. If you have 30% equity, they can sell it for 70% of its value and still cover the debt. But if you have only 5% equity and the market dips, the sale might not cover what you owe. That’s a loss for the lender - and they won’t take that risk without extra protection.

That’s why lenders use LVR. It’s not just a number. It’s their risk calculator. Lower LVR? Lower rates. Higher LVR? Higher rates, or no deal.

What If You Have Less Than 20% Equity?

You’re not stuck. But you need to adjust your plan.- Pay down your mortgage faster - Even an extra $500 a month can get you over the 20% threshold in 12-18 months.

- Get your home reappraised - If property values in your area have jumped, your equity might be higher than you think. A fresh valuation could be all you need.

- Consider a guarantor - If a family member can guarantee part of the loan, some lenders will let you remortgage with less equity.

- Look for specialist lenders - Some non-bank lenders cater to borrowers with lower equity. But watch out for fees and hidden costs.

One client in Toowoomba had only 12% equity but needed funds for a roof replacement. She used a specialist lender with a 90% LVR product. Her interest rate was 0.8% higher than standard, but she got the cash she needed and paid it off in 18 months. That’s a trade-off worth making - if you’re clear on the cost.

How Much Equity Do You Need to Cash Out?

If you’re remortgaging just to get a better rate, your equity needs are straightforward: hit that 20% threshold.But if you want to take cash out - say, $50,000 for renovations or to pay off credit cards - you need more equity.

Most lenders cap cash-out remortgages at 80% LVR. So if your home is worth $750,000, they’ll lend you up to $600,000 total. If you currently owe $400,000, you can take out up to $200,000 in cash - as long as your new loan doesn’t exceed $600,000.

Some lenders allow up to 85% LVR for cash-out, but only if you have a high income, excellent credit, and a stable job. Anything beyond that? Forget it. Australian regulators cracked down hard on high-LVR cash-outs after the 2020 property boom.

How to Check Your Equity Right Now

You don’t need an app or a financial advisor. Just do this:- Find your current mortgage balance - check your online statement or call your lender.

- Get a free estimate of your home’s value. Use realestate.com.au or domain.com.au - look at sold prices for similar homes in your suburb.

- Subtract your loan balance from your home’s estimated value. That’s your equity.

- Divide your loan balance by your home value. Multiply by 100. That’s your LVR.

Example: Your home is worth $720,000. You owe $550,000. Your equity is $170,000. Your LVR is 76.4% - well within the 80% limit. You’re in a good position to remortgage.

What Else Do Lenders Look At?

Equity isn’t the only thing. Even if you have 30% equity, you still need to pass their checks:- Income stability - Do you have a steady job? Are you self-employed with two years of tax returns?

- Debt-to-income ratio - If you have credit cards, car loans, or personal loans, your monthly repayments matter. Lenders want your total debt payments under 35-40% of your income.

- Credit score - A score below 600 will limit your options. Above 750? You’ll get the best rates.

- Property type - Units, townhouses, and rural properties are harder to remortgage than freestanding homes.

One woman in Logan City had 35% equity but was turned down because she’d just changed jobs. Her new employer was a startup. The lender didn’t know if she’d still be there in six months. She waited three months, got payslips from her new role, and re-applied - and got approved with a lower rate than before.

When to Wait Instead of Remortgaging

Not every homeowner should remortgage. Here’s when you should hold off:- You’re within 12 months of your current loan’s fixed rate ending - wait for the new rate.

- Your home value has dropped in the last year - you might have less equity than you think.

- You’re planning to move in the next 2-3 years - remortgage fees aren’t worth it unless you’ll save $5,000+ over that time.

- You’re using it to fund lifestyle spending - vacations, new cars, or shopping. That’s not wealth building. That’s debt trading.

Remortgaging isn’t magic. It’s a financial tool. Use it to reduce costs, fix your home, or pay off expensive debt. Don’t use it to chase short-term comfort.

How to Start the Process

If you’re ready:- Check your current loan balance and home value.

- Calculate your LVR. If it’s under 80%, you’re in the game.

- Compare at least three lenders - banks, credit unions, and specialist lenders.

- Ask about fees: application fees, valuation fees, discharge fees. Some lenders offer fee-free remortgages.

- Get a pre-approval in writing. It locks in your rate for 90 days.

Don’t just go to your current lender. They might not offer you the best deal. One Brisbane couple switched from Westpac to a regional credit union and saved $1,200 a year on interest - with no change to their repayments.

Final Thought: Equity Is Power

Your home equity isn’t just a number on a statement. It’s leverage. It’s control. It’s the difference between being stuck with a bad rate and having options.If you’ve got 20% or more, you’re in a strong position. Use it wisely. If you’re below that, don’t panic. Build your equity. Wait for the market. Pay down your loan. The door will open - but you need to be ready when it does.

Can I remortgage with less than 20% equity in Australia?

Yes, but it’s harder. Some lenders allow up to 90% LVR (10% equity), but you’ll pay higher interest, fees, or lenders mortgage insurance (LMI). These deals are rare and usually require strong income, excellent credit, and a stable job. Most mainstream lenders stick to 80% LVR as the standard.

How do I calculate my home equity?

Subtract your current mortgage balance from your home’s estimated market value. For example, if your home is worth $700,000 and you owe $450,000, your equity is $250,000. To find your loan-to-value ratio (LVR), divide your loan by the value and multiply by 100: (450,000 ÷ 700,000) × 100 = 64.3% LVR.

Does remortgaging affect my credit score?

It can, temporarily. When you apply, the lender does a hard credit check, which may drop your score by 5-10 points. If you’re approved and pay your new loan on time, your score will recover - and could even improve. But applying to multiple lenders in a short time can hurt your score more.

Can I remortgage if I’m self-employed?

Yes, but you’ll need more documentation. Most lenders require two years of tax returns, notices of assessment, and bank statements showing consistent income. Some specialist lenders offer low-doc options, but expect higher rates. Stability matters more than income size.

What are the costs of remortgaging?

Typical costs include application fees ($500-$1,000), valuation fees ($300-$600), discharge fees from your old lender ($200-$400), and legal or settlement fees ($500-$1,200). Some lenders waive these fees as a promotion. Always ask for a full fee breakdown before applying.

Should I remortgage to pay off credit card debt?

It can be smart - if you have enough equity and a plan. Credit cards often charge 20%+ interest. A mortgage might be 5-6%. But only do this if you won’t run up the credit card balance again. Otherwise, you’re just trading one debt for a bigger one with a longer repayment term.

How long does the remortgage process take?

Typically 3-6 weeks. The fastest approvals take 2-3 weeks if you have all documents ready. Delays usually come from property valuations, lender backlogs, or missing paperwork. Get your payslips, tax returns, and bank statements ready before you apply.