Life Insurance Premium Calculator

Calculate Your Monthly Premium

Estimated Monthly Cost

Based on article data from 2023

How This Works

Premiums vary based on age, health, gender, location, and term length. This calculator uses data from the article to show realistic estimates.

Key Factors Explained

If you're wondering how much a $100,000 life insurance policy costs each month, you're not alone. Many people start with this number because it feels like a solid, manageable amount - enough to cover final expenses, small debts, or help a family get through a rough few months. But the truth is, there’s no single answer. The monthly price can swing from under $10 to over $50, and it all depends on who you are, where you live, and what kind of policy you pick.

What You’re Actually Buying

A $100,000 life insurance policy isn’t a savings account or an investment. It’s a contract. You pay a monthly premium, and if you die during the term, your beneficiaries get $100,000. That’s it. No cash value. No growth. Just protection. Most people who buy this amount go with a term life insurance policy, which lasts 10, 20, or 30 years. It’s the cheapest, simplest option for coverage.

Why not whole life? Because whole life costs 5 to 10 times more. For the same $100,000, you might pay $100 a month or more - and you still don’t get back what you paid unless you cancel or borrow against it. For most families, term life is the smart play.

How Age Changes the Price

Age is the biggest factor. A 25-year-old in good health might pay $9 a month for a 20-year, $100,000 term policy. That’s less than a daily coffee. By 40, that same policy jumps to about $18. At 50, it’s closer to $40. And if you wait until 60? You’re looking at $80 to $100 a month - sometimes more.

Why the jump? Life insurers look at mortality risk. The older you are, the more likely you are to die during the policy term. That means they have to charge more to cover the risk. It’s not personal - it’s math.

Health Matters More Than You Think

Even one health issue can double your premium. Smoking? Add 50% to 100% to your rate. High blood pressure? Maybe a 30% increase. Being overweight? Could add $5 to $15 a month. Diabetes? You might still qualify, but your price could be 2 to 3 times higher than someone with perfect health.

Some people skip the medical exam and get “simplified issue” or “guaranteed issue” policies. They’re easier to get, but they cost way more. A $100,000 guaranteed issue policy for a 55-year-old could run $120 a month. That’s not a bargain - it’s a trap.

Gender and Location Play a Role

Women usually pay less than men for the same coverage. Why? On average, women live longer. That means the insurer is less likely to pay out during the policy term. A 35-year-old woman might pay $12 a month for a 20-year term. A man the same age? Around $15.

Location matters too. Insurance rates vary by state. A policy in Vermont might cost $14 a month. In Mississippi? $18. Why? It’s a mix of state regulations, healthcare costs, and how many insurers compete in that market. If you’re in a state with few options, prices go up.

Term Length Changes Everything

Choosing a 10-year term vs. a 30-year term changes your monthly bill. A 30-year term locks in your rate for longer - but it costs more upfront. For a healthy 30-year-old, here’s what you might pay:

- 10-year term: $7/month

- 20-year term: $12/month

- 30-year term: $18/month

Why not just pick the longest term? Because if you don’t need coverage that long, you’re overpaying. If you’re 30 and have a 10-year-old, a 20-year term might be perfect - it covers them until they’re 30 and likely independent. If you’re 45 with no kids, a 10-year term might be enough to cover a mortgage or funeral costs.

What You’re Not Paying For

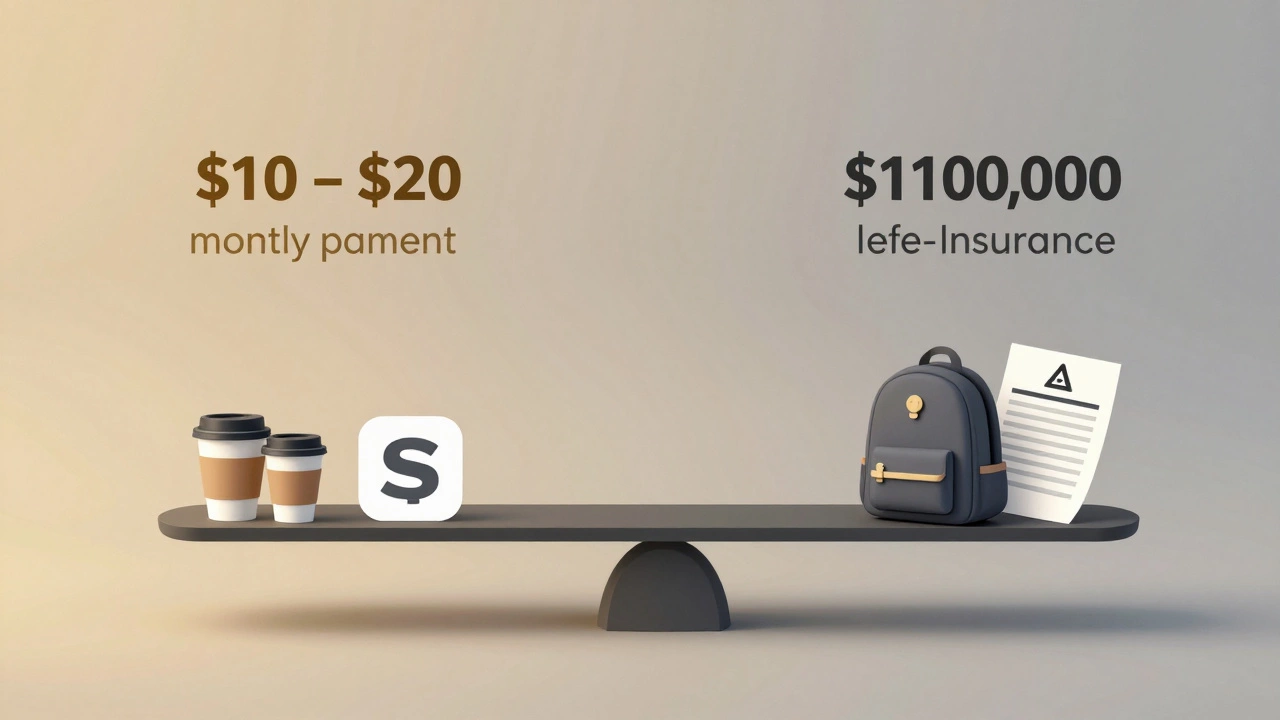

Many people think life insurance is expensive because they compare it to car insurance or health insurance. But here’s the reality: $100,000 in life insurance is one of the most affordable financial products out there. For the cost of a streaming service, you can protect your family from a financial crisis.

You’re not paying for:

- Investment returns

- Cash value growth

- Policy loans

- Dividends

You’re paying for one thing: peace of mind. If you die tomorrow, your loved ones get $100,000. No taxes. No delays. No questions.

Who Actually Needs $100,000?

Not everyone needs this much. If you’re single with no dependents, $50,000 might cover your funeral and outstanding bills. If you’re a parent with two kids and a mortgage, $100,000 might barely cover a year of childcare and lost income.

Here’s a quick rule of thumb: Multiply your annual income by 5 to 10. If you make $40,000 a year, you probably need $200,000 to $400,000. But if you’re just starting out, or you’re on a tight budget, $100,000 is a great place to start. It’s better than nothing.

How to Get the Best Rate

Shop around. Don’t just take the first quote. One insurer might offer you $15 a month. Another might offer $11. That’s $48 a year - enough to cover a weekend getaway.

Get quotes from at least three companies. Use online tools like Policygenius, Quotacy, or LifeAnt. They compare dozens of carriers at once. You don’t need to talk to an agent. You can do it all online in under 20 minutes.

Also, apply when you’re healthy. If you’ve been meaning to quit smoking, lose weight, or get your blood pressure under control - do it before you apply. Even a 10-point drop in your systolic pressure can save you $5 a month.

What Happens When the Term Ends?

Term life insurance doesn’t last forever. When the 20 or 30 years are up, your coverage stops. You can renew - but your rates will skyrocket. A 40-year-old who renews at 60 might pay $150 a month for the same $100,000.

That’s why most people don’t renew. They either:

- Have paid off their mortgage

- Have kids who are financially independent

- Have built up savings or other assets

- Switched to a smaller policy

If you still need coverage after the term ends, you can buy a new policy - but it’ll cost more because you’re older. Plan ahead.

Real Example: A 38-Year-Old Mom

Meet Sarah. She’s 38, non-smoker, healthy, lives in Ohio. She has two kids, ages 7 and 10. Her husband makes $65,000 a year, but she’s the one who handles childcare and household logistics. If she dies, her husband would need to hire help - and that costs $2,000 a month.

She gets a 20-year, $100,000 term policy. Her monthly premium? $13.50. That’s less than $1 a day. She pays it automatically from her checking account. No one even notices it’s there.

She doesn’t need $500,000. She needs enough to cover the next 10 years until her youngest is in college. $100,000 does that. And it’s affordable.

Bottom Line

$100,000 in life insurance doesn’t have to cost a fortune. For most healthy people under 50, it’s under $20 a month. Even at 60, you can find options under $70. The key is to get a term policy, stay healthy, and shop around. Don’t let fear or confusion stop you. The right policy is out there - and it’s cheaper than you think.

Is $100,000 enough life insurance?

It depends. For someone with no dependents, minor debts, or a small funeral, $100,000 is plenty. For a parent with young kids, a mortgage, or high childcare costs, it might be too little. A good rule is to aim for 5 to 10 times your annual income. If you make $40,000, you’d ideally have $200,000 to $400,000. But $100,000 is still a solid starting point if you’re on a budget.

Can I get $100,000 life insurance without a medical exam?

Yes, but it’s not ideal. Policies with no medical exam - called simplified issue or guaranteed issue - are easier to qualify for if you have health issues. But they cost 2 to 4 times more. A 50-year-old might pay $80 a month instead of $25. Only go this route if you’re denied coverage elsewhere or have serious health conditions that make standard policies impossible.

Do I need life insurance if I’m single?

You don’t need it for dependents, but you might still want it. If you have student loans, credit card debt, or co-signed loans, life insurance can cover those so your family doesn’t inherit them. It can also pay for funeral costs, which average over $9,000. Even $50,000 to $100,000 can prevent your loved ones from having to pay out of pocket.

How long should my term be?

Match the term to your biggest financial obligation. If you have a 25-year mortgage, get a 30-year term. If you have young kids, get a term that lasts until they’re 22 or 25. If you’re 50 and want to cover funeral costs, 10 years is enough. The goal is to cover your responsibilities - not extend coverage longer than needed.

Can I change my $100,000 policy later?

You can’t change the amount on an existing term policy, but you can buy a new one. If your income grows or you have another child, you can apply for a second policy. Many people start with $100,000 and later add another $200,000. Just make sure you can afford the combined premiums. Don’t over-insure.