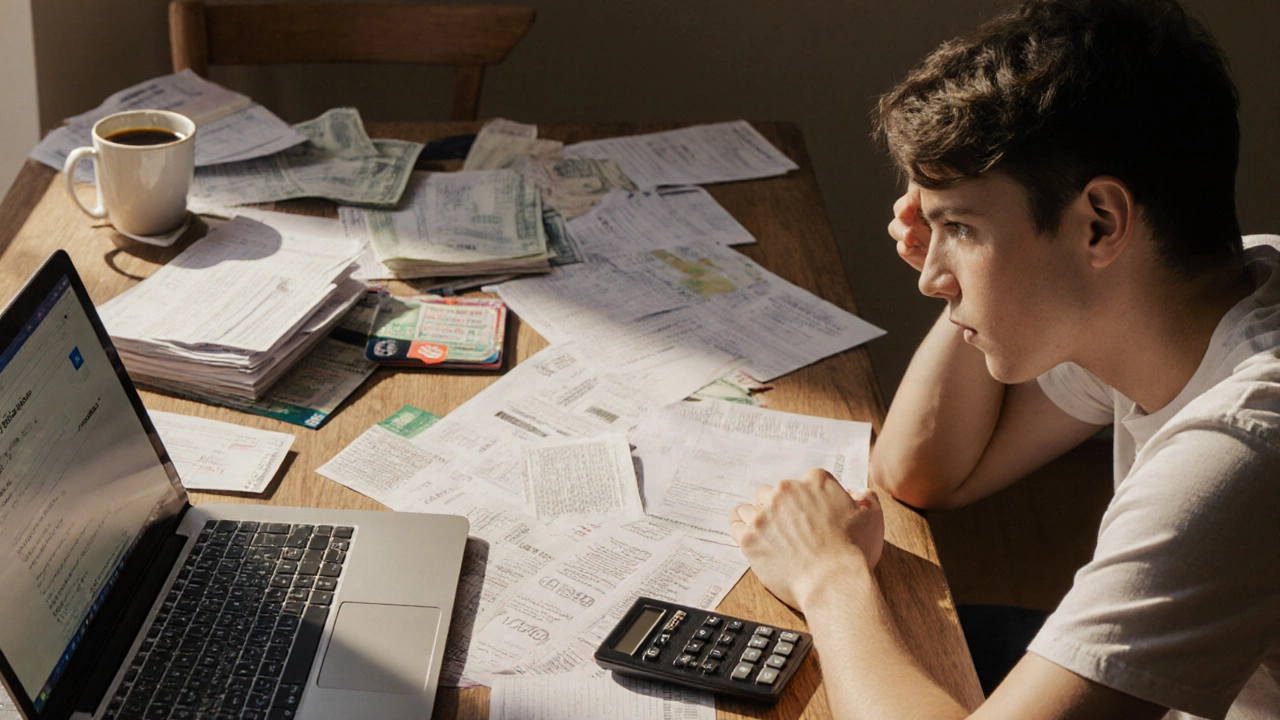

Debt Consolidation Cons: The Real Drawbacks You Should Expect

When you start looking at debt consolidation cons, the potential downsides of combining several debts into one loan, the first thing that comes to mind is convenience. But convenience often hides costs. This page breaks down the most common pitfalls so you can decide if consolidating fits your situation.

One of the biggest hidden impacts is on your credit score, the numeric representation of your borrowing history used by lenders. Opening a new consolidation loan creates a hard inquiry and adds a fresh account, which can drop your score by a few points. At the same time, closing older accounts reduces your credit age, another factor that lenders consider. In short, debt consolidation cons often include a short‑term credit hit that can affect future loan approvals.

Another frequent drawback involves interest rates, the percentage charged on borrowed money over time. While some lenders advertise low introductory rates, many consolidate high‑interest credit‑card debt with a loan that has a higher long‑term APR. The result is that you may end up paying more interest over the life of the loan than you would have by paying each debt separately. This demonstrates how debt consolidation cons can lead to higher total interest costs.

Fees are also a major consideration. Most consolidation offers come with origination fees, up‑front charges that can be a percentage of the loan amount or prepayment penalties if you clear the balance early. These costs are added to the principal, meaning you start the repayment schedule with a larger debt than you originally thought. The presence of fees is a clear example of debt consolidation cons that increase the overall financial burden.

Long‑Term Debt Management Risks

Beyond the numbers, there are behavioral risks. Consolidating can give a false sense of security, leading some borrowers to resume old spending habits because the debt appears "handled." This can cause the balance to rise again, turning a single payment into a never‑ending cycle. In this way, debt consolidation cons extend beyond the loan terms and touch on personal finance discipline.

Putting all these pieces together, you’ll see that debt consolidation cons touch credit health, interest expenses, fees and even spending behavior. debt consolidation cons are not just a list of negatives; they are factors that interact and can shape your overall financial picture. Below you’ll find articles that dive deeper into each of these areas, from credit‑score effects to fee breakdowns, so you can weigh the trade‑offs with full insight.

Negative Effects of Debt Consolidation Explained

Explore the hidden costs, credit‑score impact, longer terms, and stress that debt consolidation can bring, plus tips to avoid the pitfalls.