Debt Limits: What You Can and Can't Borrow, and How to Stay Safe

When we talk about debt limits, the maximum amount of money you’re allowed to borrow based on your income, credit history, and lender rules. Also known as borrowing capacity, it’s not just a number on a screen—it’s the line between financial breathing room and stress. Most people don’t realize their debt limit isn’t set by them. It’s set by lenders using your credit score, a three-digit number that tells lenders how risky you are to lend to. Also known as FICO score, it’s the gatekeeper for everything from car loans to home equity lines. If your score’s below 650, your debt limit might be tiny—or zero. If it’s above 750, you could qualify for five times what someone with the same income but a lower score can get.

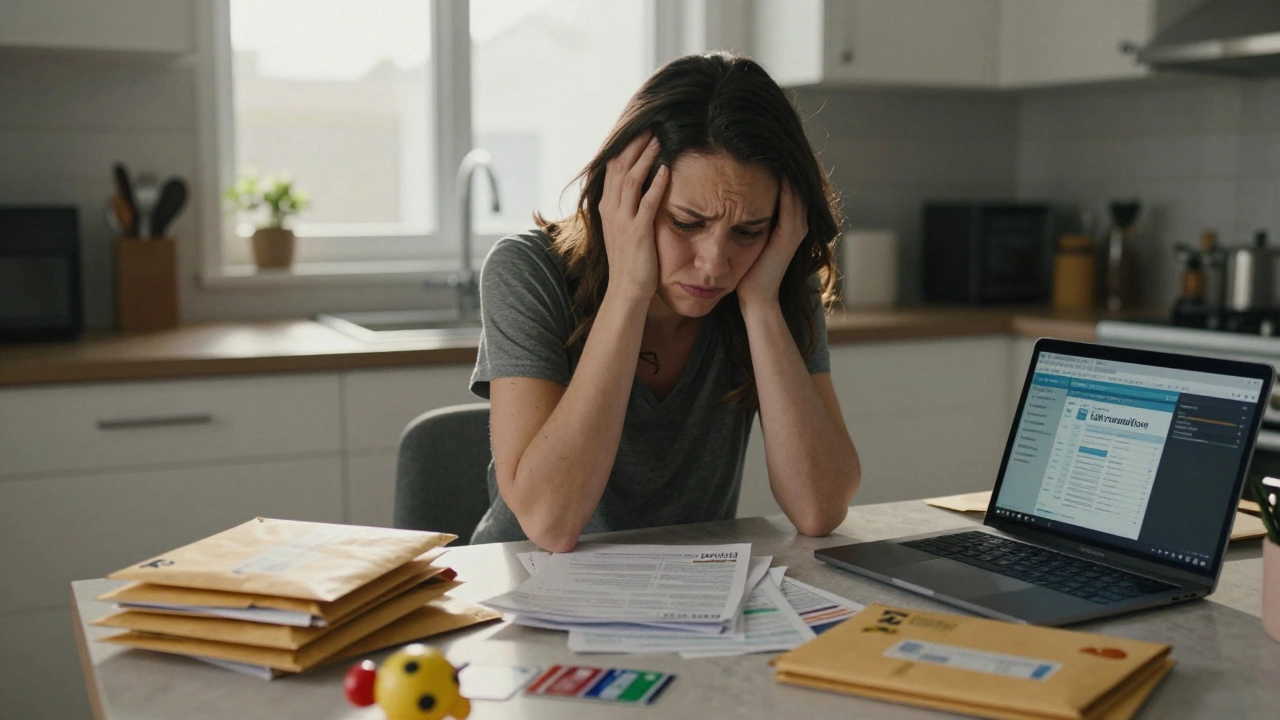

Your debt consolidation, the process of combining multiple debts into one loan with a single payment. Also known as debt merging, it’s often used when people hit their debt limit and need to simplify. But here’s the catch: consolidation doesn’t erase debt. It just rearranges it. And if you keep spending after you consolidate, you’re not fixing anything—you’re digging deeper. That’s why lenders watch your credit utilization closely. If you’re using 80% of your available credit on cards, even a high income won’t help you get a new loan. They see you as already stretched thin.

Debt limits aren’t the same for everyone. A teacher with steady pay and a 780 score might get approved for a $50,000 personal loan. A gig worker with the same score might get $15,000 because their income isn’t predictable. And if you’re trying to pull equity out of your home, your loan-to-value ratio becomes part of the equation. Most lenders won’t let you borrow more than 80% of your home’s value without private mortgage insurance. That’s a hard debt limit too.

What you’re seeing in these posts isn’t random. It’s the real-world result of people hitting their debt limits and trying to climb out. Some used loans to pay off credit cards. Others figured out how to lower payments without refinancing. A few learned why their credit score didn’t move even after paying down balances. And one thing’s clear: knowing your debt limit isn’t about chasing more credit. It’s about understanding what you can actually handle—and avoiding the traps that make people feel trapped.

Below, you’ll find honest, no-fluff guides from people who’ve been there. No sales pitches. Just what works when you’re up against your debt limit and need a real plan.

How Much Debt Is Too Much to Consolidate? A Realistic Guide for Australians

Learn when debt consolidation helps or hurts. Find out your debt-to-income ratio, avoid common traps, and discover if you're ready to truly get out of debt - not just rearrange it.