50/30/20 Budget Calculator

Enter Your Details

Enter your income to see how the 50/30/20 rule applies to your life.

You know you should track your money. You’ve probably downloaded an app, stared at a spreadsheet, or scribbled numbers on a napkin after a dinner out. But when it comes to actually sticking to a plan, most people hit a wall. The problem isn’t that you’re bad with money. It’s that you’re trying to follow a rigid system that doesn’t fit your life.

A good basic budget isn’t about restricting every penny until you feel deprived. It’s about giving yourself permission to spend freely in certain areas while ensuring the essentials are covered and your future self is taken care of. If you’re looking for a framework that works without driving you crazy, you’re in the right place. Let’s break down what a solid budget looks like and how to build one that sticks.

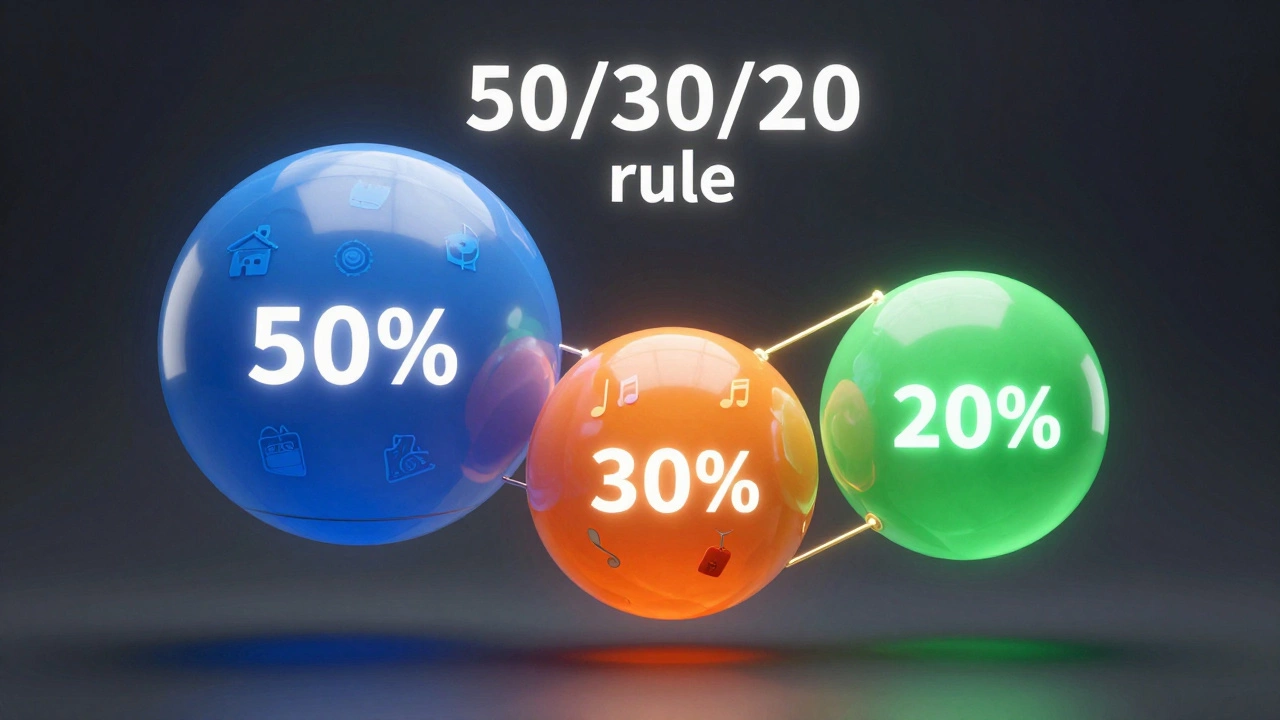

The Golden Standard: The 50/30/20 Rule

When financial experts talk about a "good" budget, they almost always point to the 50/30/20 rule, which is a simple spending framework created by Senator Elizabeth Warren to help households manage their income effectively. It splits your after-tax income into three buckets. This isn’t just theory; it’s a practical heuristic that removes the guesswork from daily decisions.

- 50% for Needs: These are non-negotiables. Rent or mortgage, utilities, groceries (not dining out), insurance, minimum debt payments, and transportation. If you can’t survive without it, it’s a need.

- 30% for Wants: This is your fun money. Streaming subscriptions, hobbies, eating out, travel, and new clothes. This category prevents burnout because it acknowledges that life is more than just paying bills.

- 20% for Savings and Debt Repayment: This goes toward emergency funds, retirement accounts (like a Superannuation fund in Australia), and extra payments on high-interest debt.

Why does this work? Because it’s flexible. If you earn $4,000 a month, you know exactly how much room you have for a night out ($1,200 total for wants) before you start encroaching on your savings. It turns abstract anxiety into concrete numbers.

Adjusting for Reality: When 50/30/20 Doesn’t Fit

Life rarely fits neatly into percentages. Maybe you live in a city where rent takes up 60% of your income. Maybe you’re debt-free and want to save more aggressively. A good budget adapts to your specific context.

If your needs exceed 50%, you have two choices: cut wants or increase income. There is no magic third option. For example, if rent eats 60% of your paycheck, your wants might shrink to 15% and savings to 25%. That’s still a valid budget. The key is intentionality. You aren’t overspending; you’re reallocating based on constraints.

Conversely, if you have low fixed costs, don’t let your wants balloon to 70%. Use that surplus to accelerate your 20% bucket. Pay off credit cards faster or invest in index funds. The goal is always progress, not perfection.

Step-by-Step: Building Your First Budget

Creating a budget doesn’t require expensive software. In fact, pen and paper often work better because the physical act of writing slows you down and makes the numbers feel real. Here is how to set it up in under an hour.

- Calculate Your Net Income: Look at your last three pay stubs. What actually hits your bank account? Don’t use your gross salary. Use the number you can spend.

- List Fixed Expenses: Write down every bill that stays the same each month. Internet, phone, car payment, insurance premiums. Add these up. This is your baseline "need."">

- Estimate Variable Needs: Groceries and gas fluctuate. Check your bank statements from the last three months. Average them out. Be honest-if you spent $800 on food last month, don’t write $400 unless you plan to cook drastically differently.

- Assign Your Wants: Decide how much you want to spend on leisure. Set a hard limit. If you go over, you must take it from another category next month.

- Automate Savings: Set up a transfer for your 20% bucket to happen on payday. If you don’t see the money, you won’t miss it.

The Hidden Trap: Lifestyle Creep

One reason budgets fail is lifestyle creep. You get a raise, so you upgrade your apartment. You get a bonus, so you buy a new car. Your income goes up, but your savings rate stays flat. A good budget protects you from this.

When your income increases, keep your "needs" and "wants" roughly the same. Direct the entire raise into your savings and debt repayment bucket. If you make $500 more a month, that’s $6,000 a year. Over ten years, invested wisely, that compounds significantly. Resist the urge to normalize higher spending immediately.

Tracking Without Obsession

You don’t need to log every coffee purchase to succeed. That level of detail leads to fatigue. Instead, use the "envelope method" digitally. Open separate sub-accounts or use tags in your banking app for different categories.

Check your balance once a week, not every day. Ask yourself: "Did I stay within my limits for groceries?" If yes, great. If no, adjust for the rest of the month. Budgeting is a feedback loop, not a punishment. If you overspend on dining out in March, reduce your clothing budget in April. Flexibility keeps you engaged.

| Strategy | Best For | Pros | Cons |

|---|---|---|---|

| 50/30/20 Rule | Most adults | Simple, balanced, easy to remember | Rigid for high-cost living areas |

| Zero-Based Budget | Debt payers, tight margins | Every dollar has a job, highly detailed | Time-consuming, requires discipline |

| Pay Yourself First | Savers, investors | Builds wealth automatically | Can lead to cash flow shortages if not careful |

Common Mistakes to Avoid

Many people abandon budgeting because they make structural errors early on. Avoid these pitfalls to ensure longevity.

- Ignoring Irregular Expenses: Car registration, birthday gifts, and holiday shopping don’t happen every month, but they happen every year. Divide these annual costs by 12 and set aside that amount monthly. This prevents credit card debt during peak seasons.

- Being Too Restrictive: If your budget feels like a prison, you will break out. Include a small "guilt-free" fund for spontaneous purchases. If you remove all joy, the system collapses.

- Not Reviewing: Life changes. So should your budget. Review your categories quarterly. Did you stop going to the gym? Move that money to savings. Did you start dating more? Adjust your entertainment budget accordingly.

Tools That Help, Not Hinder

Technology can simplify tracking, but don’t let it become a distraction. Apps like YNAB (You Need A Budget) or Mint offer automatic categorization, which saves time. However, free spreadsheets often provide more control. Choose a tool that you will actually open. If an app confuses you, switch to a notebook. The best tool is the one you use consistently.

Remember, a budget is a plan for your money, not a constraint on your freedom. It gives you clarity. When you know where your money is going, you stop worrying about whether you can afford things. You gain confidence. That is the true value of a good basic budget.

Is the 50/30/20 rule suitable for everyone?

Not necessarily. If you live in a high-cost area where rent exceeds 50% of your income, you may need to adjust the ratios. The principle remains the same-prioritize needs, allow for wants, and save-but the percentages should reflect your reality. For some, a 60/20/20 split might be more realistic initially.

How do I handle irregular income with a basic budget?

If you are freelance or commission-based, base your budget on your lowest expected monthly income. Treat any extra earnings as bonuses that go directly into savings or debt repayment. Create a "buffer" account equal to three months of expenses to smooth out lean months.

What should I do if I overspend in one category?

Don’t panic. Analyze why it happened. Was it an emergency or poor planning? If it was planned, adjust other categories for the remainder of the month. For example, if you overspent on dining out, reduce your entertainment budget next week. Use it as data, not failure.

Do I need to track every single purchase?

No. Tracking every coffee can lead to burnout. Focus on major categories like housing, food, and transport. Use weekly check-ins rather than daily logging. The goal is awareness, not micromanagement. If you generally stay within your limits, you are succeeding.

How long does it take to stick to a budget?

It typically takes three to six months to form a habit. The first month is often messy as you learn your actual spending patterns. By the second or third month, adjustments become easier. Consistency is key. Even if you slip up, return to the plan the next day.