25/75 Money Rule Calculator

Enter your monthly take-home pay to see how the 25/75 rule allocates your income between savings and living expenses.

Your Monthly Breakdown

You check your bank account after payday. The balance looks okay, but by the second week of the month, it’s already dipping into the red. You know you should save more, but between rent, groceries, and that one coffee shop you love, there’s never enough left over. Sound familiar? You’re not alone. Millions of people struggle to find a balance between enjoying their money today and securing their future.

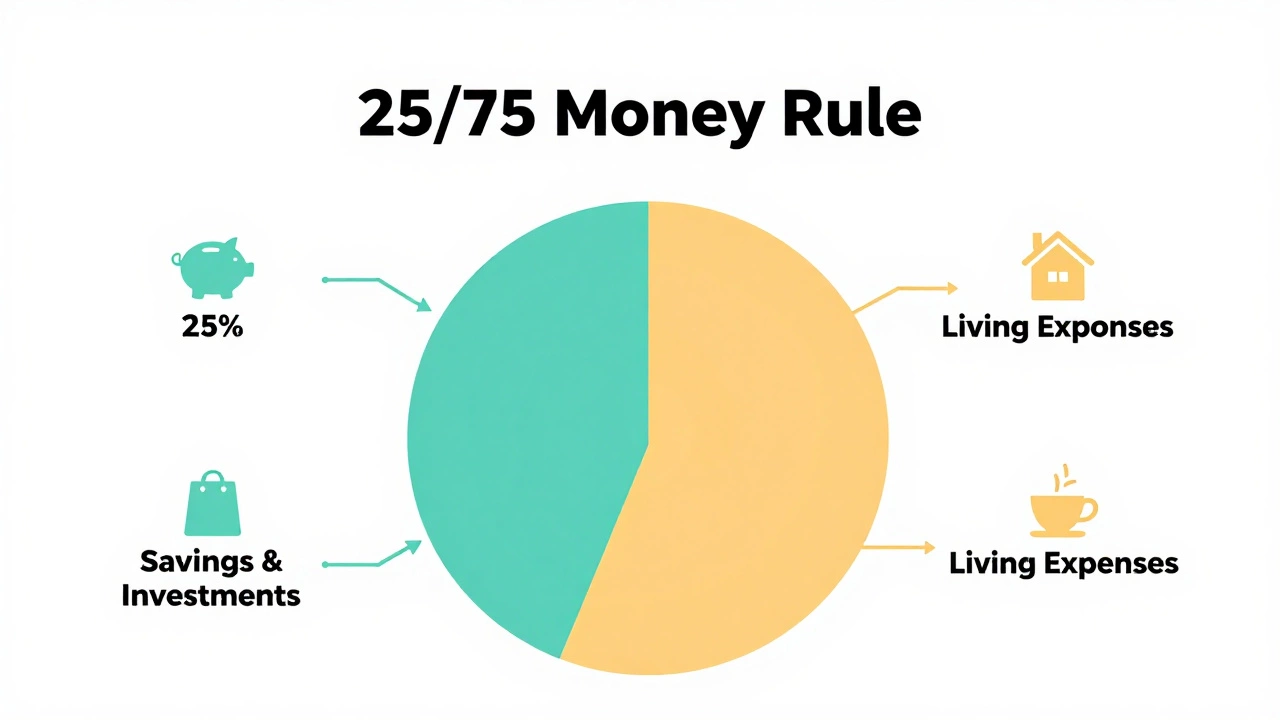

Enter the 25/75 money rule, a simple yet powerful budgeting framework that helps you allocate income without feeling deprived or overwhelmed. Unlike complex spreadsheets or rigid apps that demand constant tracking, this method splits your paycheck into two clear buckets: 25% for savings and investments, and 75% for everything else-your lifestyle, bills, and fun.

It’s not about cutting out every pleasure. It’s about giving yourself permission to spend freely on 75% of your income while still building wealth with the remaining quarter. If you’ve ever felt guilty for buying a new pair of shoes or stressed because you couldn’t afford a vacation, this rule might be the reset button your finances need.

How the 25/75 Money Rule Works

The beauty of the 25/75 rule lies in its simplicity. Instead of categorizing every single expense into needs, wants, and savings, you just divide your take-home pay into two parts. Here’s how it breaks down:

- 25% goes to savings and investments. This includes emergency funds, retirement accounts, high-yield savings, stocks, or any long-term growth vehicle. Think of this as paying your future self first.

- 75% covers all other expenses. Rent, utilities, groceries, dining out, subscriptions, hobbies-you name it. As long as it fits within this portion, you’re good.

Let’s say your monthly take-home pay is $4,000. Under the 25/75 rule, you’d set aside $1,000 for savings and investments, leaving $3,000 for living expenses. No guilt trips, no penny-pinching anxiety. Just clarity.

This approach flips traditional budgeting on its head. Most methods start with “needs” and squeeze savings into whatever’s left. The 25/75 rule starts with savings and lets you live on the rest. It forces discipline upfront but gives you freedom afterward.

Why People Are Switching to the 25/75 Rule

In a world where financial advice often feels like a maze of jargon and complicated charts, the 25/75 rule stands out for its accessibility. Here’s why so many are adopting it:

- No mental math required. You don’t need to track every latte or calculate depreciation rates. Two numbers. Done.

- Reduces decision fatigue. When you know exactly how much you can spend each month, you stop second-guessing small purchases.

- Built-in flexibility. Whether you’re renting an apartment in Sydney or owning a home in Melbourne, the percentages adjust automatically to your income level.

- Encourages consistent saving habits. By automating the 25% transfer right after payday, you build wealth passively without thinking about it.

Compare this to the popular 50/30/20 rule (which allocates 50% to needs, 30% to wants, and 20% to savings). While effective for some, the 50/30/20 model requires careful categorization. What counts as a “need”? Is streaming service a want or a necessity? These gray areas lead to confusion. The 25/75 rule eliminates ambiguity entirely.

| Rule | Savings Allocation | Complexity Level | Best For |

|---|---|---|---|

| 25/75 Money Rule | 25% | Low | Beginners, minimalists, automation lovers |

| 50/30/20 Rule | 20% | Medium | Those who want detailed spending categories |

| Zero-Based Budgeting | Variable | High | Detail-oriented planners, debt payers |

| Pay Yourself First | Custom % | Low-Medium | People focused on aggressive savings goals |

Setting Up Your 25/75 Budget Step-by-Step

Ready to try the 25/75 money rule? Follow these steps to get started:

- Calculate your take-home pay. Use your net income-the amount that actually hits your bank account after taxes and deductions. Gross salary doesn’t count here.

- Automate the 25% transfer. Set up a direct deposit split or automatic transfer from your checking account to a dedicated savings or investment account. Do this immediately after payday.

- Live on the remaining 75%. Pay bills, buy groceries, go out with friends-whatever fits within this limit. Track large purchases if needed, but avoid micromanaging small ones.

- Review quarterly. Check if your 75% is covering essentials comfortably. If you’re consistently short, consider adjusting your savings rate temporarily until your situation improves.

Pro tip: Open a separate high-interest savings account for your 25%. Watching that number grow motivates you to stick with the plan. In Australia, banks like ING and UBank offer competitive rates that make idle cash work harder for you.

Real-Life Scenarios: Who Benefits Most?

The 25/75 rule isn’t one-size-fits-all, but it shines in specific situations. Let’s look at three common profiles:

The Young Professional

Sarah, 28, earns $65,000 annually ($4,200/month take-home). She lives in Brisbane, rents a modest apartment, and loves traveling. With the 25/75 rule, she saves $1,050/month toward her superannuation and travel fund. Her $3,150 covers rent, food, and weekend adventures. She hasn’t gone into debt in two years-and her savings have grown by over $25,000.

The Freelancer

Mark, 35, works as a graphic designer. His income fluctuates, averaging $7,000/month. He uses the 25/75 rule during peak months and dips slightly below 25% in slow periods. Over time, he builds a buffer that smooths out irregular cash flow. His key insight? Consistency matters more than perfection.

The Family Planner

Emma and James, both 40, earn combined $9,000/month. They have two kids and aim to buy a home in five years. Their 25% ($2,250) goes into a home deposit fund and children’s education savings. The 75% ($6,750) handles mortgage payments, school fees, and family activities. They’ve avoided credit card debt entirely since starting.

Pitfalls to Avoid When Using the 25/75 Rule

Even simple systems have traps. Watch out for these common mistakes:

- Ignoring inflation. Saving 25% sounds great, but if your costs rise faster than your income, you’ll feel squeezed. Adjust your savings goal periodically based on cost-of-living changes.

- Mixing savings with spending accounts. Keep your 25% completely separate. Temptation kills progress. Use different banks or account types to create psychological distance.

- Failing to invest wisely. Parking your 25% in a low-interest savings account defeats the purpose. Explore index funds, ETFs, or government bonds to maximize returns.

- Not accounting for windfalls. Got a bonus or tax refund? Don’t blow it all. Add it to your 25% bucket to accelerate your goals.

Another subtle trap? Assuming 25% is always achievable. If you’re carrying significant debt, especially high-interest credit cards, prioritize paying that off before locking in strict savings ratios. Financial health comes first; optimization follows.

Adapting the Rule for Different Life Stages

Your ideal savings rate evolves with life. Here’s how to tweak the 25/75 rule across decades:

- 20s: Focus on building emergency funds and investing early. Compound interest works best when given time. Aim for 25-30% if possible.

- 30s: Balance career growth with family responsibilities. Consider increasing contributions to superannuation or private pension plans.

- 40s: Shift toward stability. Reduce riskier investments and increase liquidity. Maintain 25% unless nearing major purchases like homeownership.

- 50s+: Prepare for retirement. Maximize employer matches and explore annuities or guaranteed income streams. Savings may dip to 15-20% if drawing down assets.

Remember, the 25/75 rule is a guideline, not a law. Flexibility ensures longevity. If medical emergencies or job loss disrupt your rhythm, pause and reassess. Resuming later beats abandoning altogether.

Tools That Make the 25/75 Rule Easier

Technology can automate what used to require willpower. Try these tools:

- Split deposits via payroll. Many Australian employers allow directing portions of salary to multiple accounts. Set 25% to go straight to savings.

- Use budgeting apps likeYNAB or EveryDollar. Though designed for zero-based budgeting, they can enforce the 25/75 split visually.

- Investment platforms like CommSec or Stake. Automate regular buys into diversified portfolios using your 25% allocation.

- Savings challenges. Apps like Savee gamify putting away money, making the 25% feel less like a chore.

For those who prefer manual control, a simple spreadsheet works too. Create columns for Income, Savings (25%), Spending (75%), and Actual Spend. Update weekly to stay aligned.

FAQ

Is the 25/75 money rule better than the 50/30/20 rule?

It depends on your personality. The 25/75 rule is simpler and reduces decision fatigue, making it ideal for beginners or those overwhelmed by detail. The 50/30/20 rule offers more granularity, which suits people who enjoy tracking categories closely. Neither is inherently superior-choose what keeps you consistent.

Can I use the 25/75 rule if I’m paying off debt?

Yes, but adjust priorities. High-interest debt (like credit cards) should come before aggressive savings. Allocate part of your 25% toward extra repayments. Once debt is manageable, resume full 25% savings. Low-interest debt (student loans, mortgages) can coexist with standard 25/75 allocations.

What happens if my 75% isn’t enough to cover expenses?

Reevaluate your budget. Identify non-essential spending you can cut or renegotiate fixed costs (internet, insurance). Temporarily reduce savings to 15-20% until your situation stabilizes. Long-term fixes include raising income through side gigs or promotions rather than permanently lowering savings.

Should I save 25% of gross or net income?

Always base calculations on net income-what actually lands in your pocket. Gross figures ignore taxes and deductions, leading to unrealistic expectations. Calculators online can help convert gross to net quickly.

Does the 25/75 rule work for freelancers or variable incomes?

Absolutely. Base your 25% on average monthly earnings over six months. During high-income months, save extra to build a buffer. In lean months, dip below 25% temporarily. Consistency over time matters more than hitting exact percentages every single month.

Where should I put my 25% savings?

Start with an emergency fund in a high-interest savings account (aim for 3-6 months’ expenses). Then diversify: contribute to superannuation, open brokerage accounts for index funds, or explore term deposits for medium-term goals. Avoid keeping large sums in everyday transaction accounts due to low returns.

Can I combine the 25/75 rule with other strategies?

Yes! Pair it with envelope budgeting for discretionary spending, or use sinking funds within your 75% for upcoming big purchases (cars, holidays). Hybrid approaches often yield the best results by combining structure with adaptability.