Deposit Insurance Coverage Calculator

Check Your Savings Protection

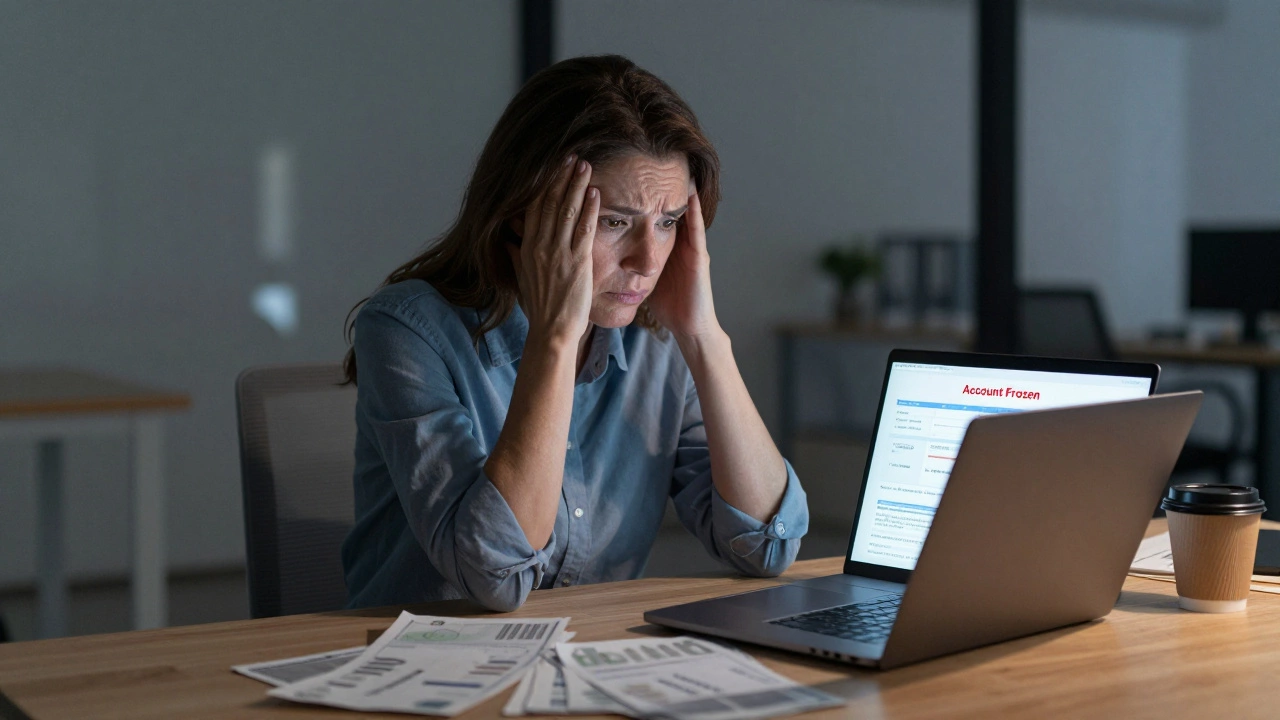

Your Protection Analysis

You have of uninsured funds. Consider spreading your savings across multiple FDIC-insured banks to protect this portion.

Your savings are fully protected within the insurance limit. Good financial practice!

Remember: Deposit insurance only covers up to $250,000 per depositor, per bank in the US. Other countries have different limits. Always confirm your bank's insurance coverage before depositing large sums.

Protect Your Savings

- Split deposits across multiple FDIC-insured banks if you have more than $250,000

- Avoid banks offering "too good to be true" interest rates

- Check your bank's Tier 1 capital ratio

- Verify if online banks are FDIC-insured

When you put money into a savings account, you expect it to be there when you need it. Not just safe, but accessible. But what happens when a bank starts to crack? In early 2026, four major banks in the U.S. and Europe showed clear signs of distress-enough to make millions of savers pause and ask: Is my money still safe?

Bank of the Midwest: The Quiet Collapse

Bank of the Midwest, a regional lender with $42 billion in assets, quietly stopped reporting its quarterly earnings in December 2025. By January, regulators stepped in. The bank had overexposed itself to commercial real estate loans-mostly office buildings left empty after remote work took hold. When tenants stopped paying, the bank’s loan portfolio began to unravel. Its Tier 1 capital ratio dropped below 5%, well under the 8% minimum regulators require. Unlike big-name failures in 2023, this one didn’t make headlines until it was too late. Over 1.2 million savings accounts were affected, but FDIC insurance covered up to $250,000 per depositor. If you had more than that, you’re still waiting for the rest.

First Continental Trust: Too Much Risk, Too Little Transparency

First Continental Trust operated like a shadow bank. It marketed itself as a high-yield savings option-offering 5.8% APY while competitors stuck to 4%. The catch? Most of its deposits were funneled into private credit funds and cryptocurrency-backed loans. When Bitcoin plunged 32% in November 2025, the bank’s collateral values collapsed. Customers noticed withdrawals were delayed. Then came the freeze. Regulators found the bank had falsified its liquidity reports for 18 months. Over 850,000 accounts were locked. The FDIC took over, but payout timelines are now stretched out to 90+ days. If you were banking with them for the extra interest, you’re now learning how risky that gamble was.

Europa Savings & Loan: The Eurozone Ripple Effect

Based in Frankfurt, Europa Savings & Loan was a favorite among expats and digital nomads for its multi-currency savings accounts. But behind the scenes, the bank had borrowed heavily in euros to fund dollar-denominated mortgages. When the European Central Bank raised rates to 4.5% in late 2025, its funding costs spiked. It couldn’t refinance. Its net interest margin turned negative. In January, the European Central Bank declared it “non-viable” and ordered a wind-down. Over 600,000 accounts were suspended. The EU’s deposit guarantee scheme covers up to €100,000 per person, but non-EU residents are left out. If you held euros, dollars, or pounds in that account-you’re now in legal limbo.

First National Bank of Nevada: The Local Giant That Cracked

First National Bank of Nevada was the backbone of Reno and Las Vegas. It had 2.3 million savings accounts, mostly from retirees and small business owners. Its downfall? Over-reliance on casino-related loans and a failed attempt to enter the crypto mining space. When Nevada’s gaming revenue dropped 19% in 2025 due to tighter federal regulations and competition from online platforms, the bank’s loan defaults surged. Its internal audit, leaked in January, showed 37% of its loan book was at risk. The FDIC seized it on January 15. While insured deposits are being paid out, the process is slow. People who relied on automatic bill payments from their savings accounts are now scrambling.

What This Means for Your Savings Account

Here’s the hard truth: not all banks are created equal. The big names-Chase, Bank of America, Wells Fargo-still have strong balance sheets. But regional banks, niche lenders, and those promising unusually high returns? They’re the ones at risk. The FDIC and similar systems overseas (like the UK’s FSCS or the EU’s DGS) only protect you up to a limit. If you’ve got $300,000 in one account? You’re uninsured for $50,000. And if that bank fails? You might wait months to get even the insured portion.

How to Protect Your Money Now

- Split your deposits-if you have more than $250,000, spread it across two or more FDIC-insured banks. Same rule applies abroad: €100,000 per bank in the EU, £85,000 per bank in the UK.

- Avoid “too good to be true” rates-if a bank offers 5%+ on savings while others are at 4%, dig deeper. Ask: What are they lending money to? What’s their capital ratio? A quick Google search for “[Bank Name] capital ratio 2025” often reveals red flags.

- Check your bank’s rating-use independent tools like Bankrate’s Safe & Sound Ratings or BauerFinancial’s 5-Star System. A 3-star or below means trouble is brewing.

- Know your deposit insurance limits-in the U.S., it’s $250,000 per depositor, per bank. In Australia, it’s AUD 250,000 per person, per authorized deposit-taking institution. If you’re holding foreign currency, confirm coverage rules.

What Happens When a Bank Fails

When a bank fails, regulators don’t just shut it down overnight. They usually sell its assets to another institution. In most cases, your insured deposits are transferred automatically. But the process isn’t instant. You might lose access for up to 10 business days. If you have a direct debit set up for rent or utilities, you’ll need to act fast. That’s why keeping a small emergency buffer in a separate, unrelated account is smart.

Uninsured funds? Those are treated like creditors. You might get some back, but it could take years. In the 2023 failures, some depositors recovered only 30-60% of their uninsured amounts. And there’s no guarantee.

Why This Isn’t Just a U.S. Problem

These four failures aren’t isolated. They reflect a global pattern: banks chasing yield, underestimating risk, and hiding exposure behind complex products. In Canada, two credit unions have frozen withdrawals after similar commercial real estate losses. In Australia, the Australian Prudential Regulation Authority (APRA) has warned regional lenders to reduce exposure to property-backed loans. If you’re using an online bank based overseas-like Revolut, N26, or Monzo-check if your deposits are covered by local insurance schemes. Many aren’t.

What to Do Today

Log into your savings account right now. Check the bank’s name. Look up its latest financial report. If you can’t find it, call customer service and ask: “What’s your Tier 1 capital ratio?” If they hesitate or give a vague answer, start moving your money. Don’t wait for headlines. By the time the news breaks, it’s too late.

Final Thought

Your savings account isn’t just a place to store money. It’s your financial safety net. When banks fail, it’s not the economy that suffers first-it’s the people who trusted them. Don’t assume safety. Verify it. Because in 2026, the safest bank isn’t the biggest one. It’s the one you understand.

Are my savings protected if my bank fails?

Yes-but only up to a limit. In the U.S., the FDIC insures $250,000 per depositor, per bank. In the EU, it’s €100,000. In Australia, it’s AUD 250,000 per person, per authorized deposit-taking institution. Anything above that is at risk. Always check your bank’s insurance coverage and spread large balances across multiple institutions.

How do I know if my bank is in trouble?

Look for three signs: unusually high interest rates on savings (over 5%), lack of public financial reports, and a low capital ratio (below 8%). Use free tools like BauerFinancial’s 5-Star Rating or Bankrate’s Safe & Sound Ratings. If your bank doesn’t publish quarterly earnings or avoids transparency, it’s a red flag.

What happens to my money if my bank is seized?

Insured deposits are usually transferred to another bank within a few business days. You’ll get a notice in the mail or via email. Uninsured funds become part of the bank’s liquidation process-you may recover some money, but it can take years. Don’t wait for news. If you suspect trouble, move your insured funds to another institution immediately.

Can online banks fail too?

Yes. Online banks like Ally, Marcus, or Chime are still FDIC-insured if they’re backed by a licensed bank. But many fintech apps (like Revolut or N26) don’t hold banking licenses themselves. Their deposits may be held by partner banks-but you need to confirm whether those partners are insured and what limits apply. Always check who actually holds your money.

Should I move my money out of a bank that’s been flagged?

If your bank is flagged by regulators, has a low capital ratio, or stopped publishing reports, yes-move your insured funds (up to $250,000) to a more stable institution. Don’t wait for a shutdown. The transfer process can take time, and you don’t want to be locked out. Use the FDIC’s BankFind tool to confirm the new bank’s insurance status before moving.