Debt Consolidation Calculator

How This Calculator Works

Enter your current debts below, then input your potential consolidation loan terms to see:

- Current total debt and average interest rate

- Estimated time to pay off debts at current rates

- Monthly payments and total interest saved

- Key risks to consider

Remember: Consolidation works only if you stop adding new debt. This calculator assumes you won't use credit cards after consolidation.

Your Current Debts

Your Potential Consolidation Loan

Feeling crushed by credit card bills, medical bills, or multiple personal loans? You’re not alone. In Australia, nearly 1 in 5 adults are carrying high-interest debt they can’t seem to escape. That’s where the idea of a debt consolidation loan comes in - but is it really a lifeline, or just swapping one problem for another?

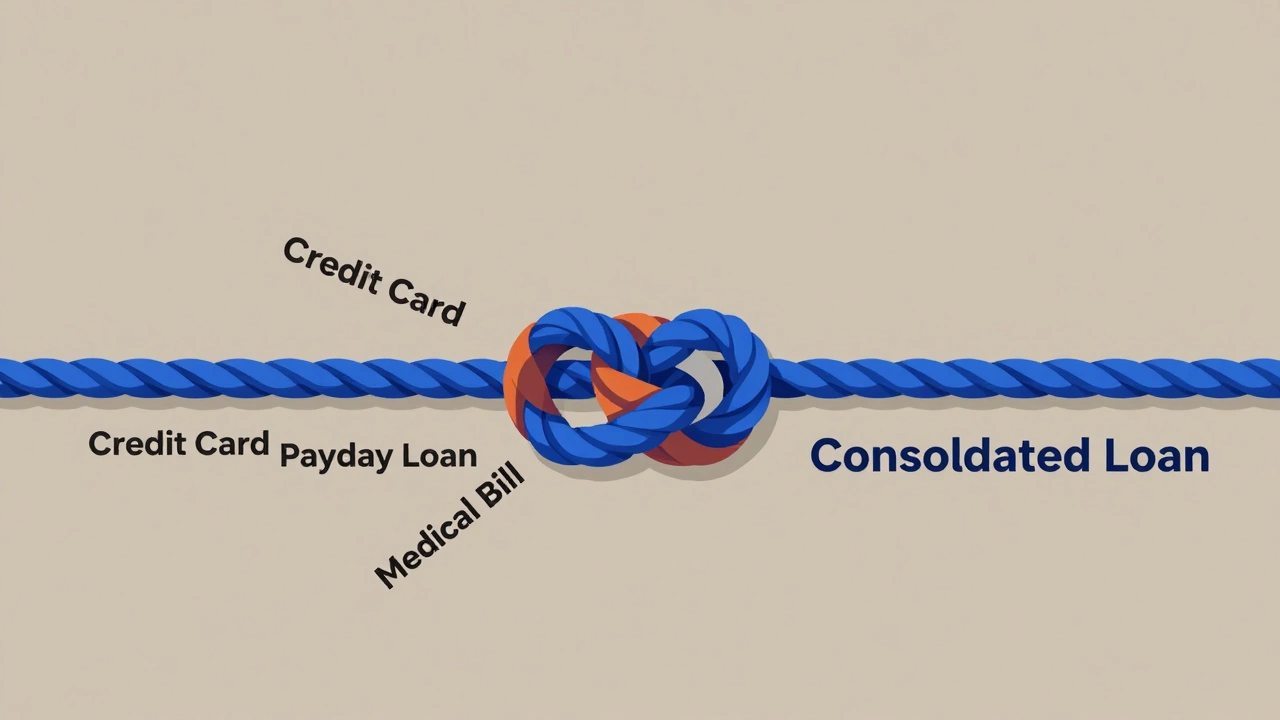

What a debt consolidation loan actually does

A debt consolidation loan isn’t magic. It doesn’t erase your debt. It just moves it. You take out one new loan - usually with a lower interest rate - and use the money to pay off several smaller, higher-interest debts. Suddenly, instead of juggling five payments a month, you’ve got one. That’s the appeal.

Think of it like this: You’ve got a $5,000 credit card balance at 22% interest, a $3,000 personal loan at 18%, and a $2,000 medical bill you paid with a buy-now-pay-later scheme at 25%. That’s $10,000 in debt, with an average rate of over 21%. Now imagine you get a $10,000 personal loan at 9.5%. You pay off all those bills, and now you’re only paying 9.5% on the whole amount. That’s a real savings - if you stick to the plan.

Who qualifies for a debt consolidation loan in 2025?

Banks and lenders aren’t handing out low-rate loans to anyone. They look at three things: your credit score, your income, and your debt-to-income ratio.

If your credit score is below 600, you’re probably looking at rates over 15%. That defeats the whole purpose. Most lenders want to see a score of at least 650 to offer the best terms. In Australia, lenders like Afterpay, Up, and Humm offer options for lower scores, but the interest rates climb fast.

Your income needs to be stable. If you’re on a casual contract or your income fluctuates, you’ll need to prove you’ve got consistent earnings over the last six months. Lenders also check your debt-to-income ratio - that’s your total monthly debt payments divided by your gross monthly income. If it’s over 40%, you’ll likely be turned down.

Here’s the reality: if you’re already maxed out on credit cards and missing payments, a consolidation loan might not be the answer. You might need to talk to a free financial counsellor first. Services like Financial Counselling Australia can help you negotiate with creditors or set up a payment plan without taking on more debt.

When a debt consolidation loan makes sense

It works best when you have:

- Multiple high-interest debts (credit cards, store cards, payday loans)

- A steady job and reliable income

- A credit score above 650

- The discipline to stop using the cards you paid off

Let’s say you’re earning $70,000 a year, have $15,000 in credit card debt at 20% interest, and you’re paying $400 a month just to keep up. At that rate, it’ll take you over 5 years to pay it off - and you’ll pay nearly $9,000 in interest.

Now, get a $15,000 personal loan at 10% over 4 years. Your monthly payment drops to $380. You save $5,000 in interest. That’s not a small win. But only if you don’t run up those credit cards again.

The hidden traps

There are three big risks most people don’t see coming.

First: Fees. Some loans charge upfront application fees, monthly service fees, or early repayment penalties. A loan with a 9% rate might sound great - until you find out there’s a $500 fee. That’s like adding 3% to your interest rate right off the bat.

Second: Longer repayment terms. You might get a lower monthly payment by stretching the loan to 7 years instead of 3. But that means you’re paying interest longer. You could end up paying more overall, even with a lower rate.

Third: False security. Paying off your credit cards feels like progress. But if you start using them again, you’re now carrying the loan AND new credit card debt. That’s a debt spiral - not a solution.

One client I worked with in Brisbane paid off $12,000 in credit card debt with a consolidation loan. Six months later, she had $18,000 in new debt. She didn’t fix her spending habits. She just moved the problem.

Alternatives to a consolidation loan

You don’t have to take out another loan to get out of debt.

- Debt management plan: A nonprofit credit counselling agency negotiates lower interest rates with your creditors. You pay one monthly amount. No new loan needed. Free in Australia through services like MoneySmart or Good Shepherd.

- Balance transfer credit card: If you have good credit, you can transfer your balances to a card with 0% interest for 12 to 24 months. Watch out for balance transfer fees (usually 1-3%) and the rate after the promo ends.

- Debt snowball or avalanche: Pay off your smallest debt first (snowball) or the one with the highest interest (avalanche). It’s slower, but it builds momentum without adding more debt.

- Government hardship programs: If you’re on Centrelink or have a sudden drop in income, you might qualify for reduced payments or temporary relief on utility bills, medical debt, or even private loans.

How to apply for a debt consolidation loan in 2025

If you’ve decided a loan is right for you, here’s how to do it right:

- Write down every debt you have: lender, balance, interest rate, minimum payment.

- Add them up. That’s how much you need to borrow.

- Check your credit report for free via Equifax or Experian. Fix any errors before applying.

- Use comparison sites like RateCity or Canstar to see what’s available. Don’t apply to five lenders at once - each application hurts your score.

- Choose the loan with the lowest total cost (not just the lowest monthly payment).

- Use the loan money ONLY to pay off your listed debts. Close the old accounts if you can.

- Set up automatic payments. Miss one, and your rate could jump.

Most lenders in Australia will give you a decision within 24 hours. Funds usually hit your account in 1 to 3 business days.

What happens if you can’t repay the consolidation loan?

If you fall behind, the consequences are serious. Unlike credit cards, personal loans are unsecured - but lenders still have legal options. They can:

- Send your account to a collections agency

- Take you to court

- Get a judgment that affects your credit score for years

If you’re struggling, don’t ignore it. Contact your lender before you miss a payment. Many will offer a temporary payment pause or reduced amount if you explain your situation. You can also call the National Debt Helpline at 1800 007 007 - it’s free and confidential.

Bottom line: Is it worth it?

A debt consolidation loan can be a smart move - if you’re disciplined, have good credit, and understand the risks. It’s not a fix for bad spending habits. It’s a tool to simplify and reduce cost - but only if you use it right.

Before you sign anything, ask yourself: "Am I changing my behaviour, or just moving my debt?" If the answer is the latter, you’re setting yourself up to be right back here in a year.

Take the time to compare options. Talk to a free financial counsellor. Run the numbers. Don’t let desperation push you into a loan that looks good on paper but traps you longer than you expected.

Can I get a debt consolidation loan with bad credit?

Yes, but your options are limited and expensive. Lenders like Jacaranda Finance or Nimble offer loans to people with credit scores under 600, but interest rates can be 25% or higher. You might pay more in interest than you save. If your credit is poor, focus on improving it first - or consider a free debt management plan through a nonprofit agency.

Will a debt consolidation loan hurt my credit score?

It can, temporarily. When you apply, the lender checks your credit - that’s a hard inquiry and can drop your score by 5 to 10 points. But if you use the loan to pay off credit cards, your credit utilization ratio drops, which usually helps your score over time. The key is making on-time payments. Miss one, and your score can drop 100+ points.

Can I consolidate student loans with a personal loan?

Technically yes, but it’s usually a bad idea. Australian government student loans (HECS-HELP) have no interest, and repayments are based on your income. If you roll them into a personal loan, you lose those protections and start paying interest immediately. Only do this if you’re paying off private student loans with high rates - never government ones.

How long does it take to pay off a debt consolidation loan?

Most personal loans for debt consolidation in Australia have terms between 2 and 7 years. Shorter terms mean higher monthly payments but less interest overall. Longer terms lower your monthly bill but cost more in the long run. Choose based on your budget - not just what looks easiest.

Do I need to use my home as collateral?

No, not for a standard debt consolidation loan. Those are unsecured. But if you’re considering a secured loan - like using your home equity - that’s a different product. Secured loans have lower rates, but you risk losing your home if you default. Only consider this if you’re absolutely sure you can repay it.

Can I get a debt consolidation loan if I’m on Centrelink?

It’s very difficult. Most lenders require income from employment, not government benefits. Centrelink payments like JobSeeker or Disability Support Pension are often not accepted as qualifying income. Your best bet is a free debt management plan through a nonprofit agency. They can help you negotiate with creditors without needing a loan.

If you’re serious about getting out of debt, start by listing every dollar you owe. Then ask yourself: "Am I fixing my habits, or just moving the problem?" The answer will tell you whether a loan is the right step - or if you need to go back to basics first.